|

Commercial Sales Summary: Back to Average

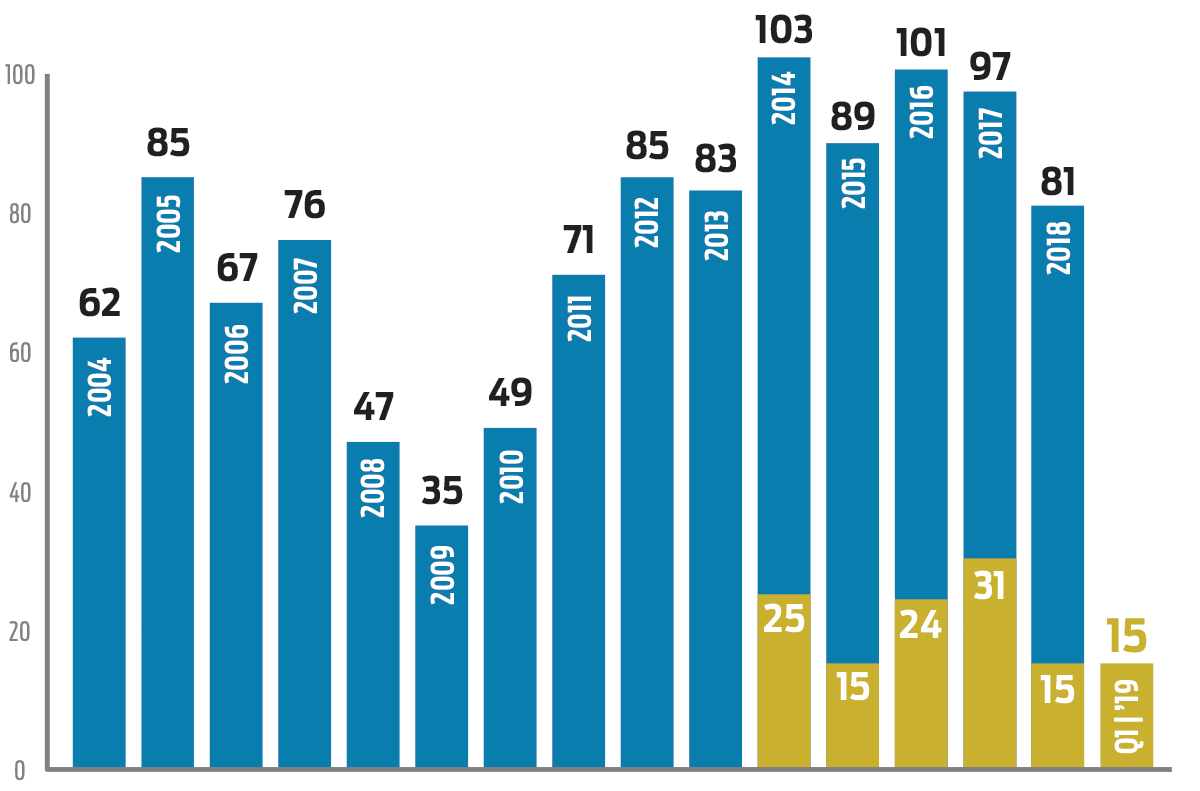

In general the number of annual sales has been on a slow decline since the market high 100+ sales in 2014 and 2016, and 2018 in particular saw the fewest sales since 2011. On the upside, Q1 sales volume this year is over double Q1 2018.

It seems like we are getting back to sales volume figures close to or slightly below our historic averages. Over a 15-year period we have averaged almost 19 sales per quarter for a total of roughly 75 sales per year. Case in point, last year there was a total of 81 sales compared to 97 sales for 2017. This year’s Q1 consisted of 15 sales compared to 14 for Q1 2018. The asterisk for Q1 2018, of course, was the negative effect of the fires and mudslides on sales activity.

Dollar volume for Q1 2019 was also up, totaling just under $104 Million in sales volume compared to Q1 2018 which totaled $53 Million. However, keep in mind that first quarters historically do not always set the tone for performance for the rest of the year.

In general the number of annual sales has been on a slow decline since the market high 100+ sales in 2014 and 2016, and 2018 in particular saw the fewest sales since 2011. On the upside, Q1 sales volume this year is over double Q1 2018. This year’s sales volume included major office/R&D buildings totaling $65.8 Million of the total $104 Million. This included the sale of 4050 Calle Real in Santa Barbara, an office building that was purchased by the tenant, Cencal Health, for $30.5 Million; 600 Pine Ave. in Goleta, which houses ATK as a tenant and sold for $21.5 Million to investors; and 454 S. Patterson Ave. in Goleta which sold in an Off Market deal for an undisclosed figure.

Based on the numbers the demand for office is still strong in Santa Barbara with a total of eight (8) sales. Industrial sales followed with a total of four (4) sales and a sales volume of $28 Million, then retail with two (2) sales totaling $4.3 Million, and finally one land sale totaling $5.1 Million.

|

Conservative Investors

The number of investors purchasing buildings cooled off this quarter, accounting for only five (5) sales or 33% of all sales. In general, investors are analyzing property returns more critically and looking for more secure investments in anticipation of a softer market near term.

Bullish Owner-Users

Remarkably we have seen a steadily increasing trend of owner-users purchasing properties over the last few quarters and this quarter is no different. Of the 15 sales this quarter, 10 were purchased by owner-users which equates to 66% of all sales. It is our opinion that more owner-users are looking long-term and taking advantage of low interest rates.

Notable Large Sales

As mentioned previously, a large portion of the sales volume this quarter is attributable to just three (3) large sales. For whatever reason we have been seeing larger individual sales as some of these properties have recently come to market and a combination of cash and financing have been available for these purchases.

|

Leasing Summary: Office vacancy rate climbs to highest level in Santa Barbara since 2003

Office

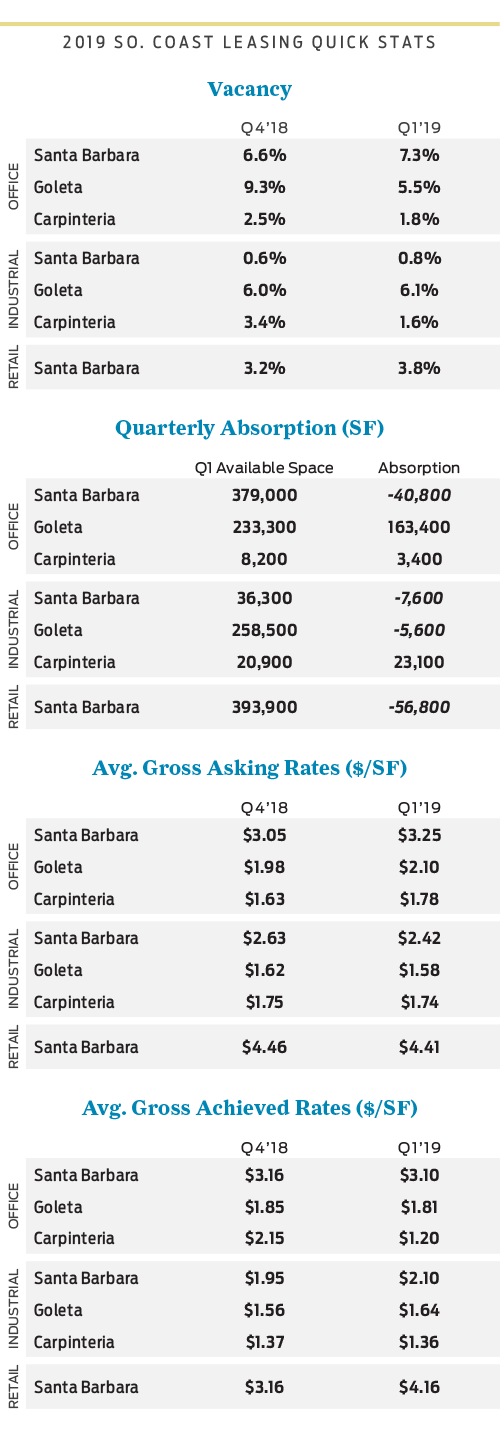

Santa Barbara’s office sector offered the most notable story in South Coast leasing activity during Q1 as the vacancy rate ratcheted up to 7.3%, its highest level since the 7.9% recorded in the Summer of 2003. This constitutes about 379,000 SF from 123 available properties. A higher than usual 29 spaces totaling more than 100,000 SF came to market during Q1 (26% of all available square footage) including a few larger spaces at 402 E. Gutierrez (26,339 SF) and 3820 State St. (10,604 SF), with 17 spaces coming online in January alone. Spaces between 1,500–3,000 SF continue to make up the vast majority of vacancies, and many spaces that are in need of improvements, have constrained parking or are in a one-off location continue to sit vacant.

Larger companies such as Invoca, Honey Sciences and a few others have recently gobbled up some of the larger available properties, leaving few spaces above 5,000 SF in size. Achieved lease rates for Q1 averaged $3.10/SF Gross, slightly down from $3.16/SF Gross in Q4 ‘18. While the average gross asking rate increased over previous quarters to $3.25/SF Gross, this hike was pushed by a handful of properties with much higher asking rates, including some smaller availabilities in Santa Barbara and a few spaces in Montecito. Ultimately with the increase in vacancies we may actually see asking rates and achieved rates come down over the next quarter.

Goleta experienced a significant drop in office vacancy with approx. 143,700 SF leased in Q1 ’19, or about 36% of total available space, bringing the vacancy rate down to 5.5%. That said, it must be noted the Apeel Sciences lease at 71 S. Los Carneros Rd. accounted for 105,000 SF, or 73% of total square footage leased. In smaller markets like Goleta, one large lease or vacancy can dramatically shift the perspective. Still, this drop in vacancy can be viewed as a positive sign for Goleta’s economy, especially with a number of tech giants searching for locations to bring more skilled labor to the area. Office/R&D leasing should remain steady through 2019, with an increase in inventory forecast for 2020 when RAF Pacifica completes the five new buildings at Cabrillo Business Park, totaling an additional 145,000 SF.

Meanwhile in Carpinteria, the office vacancy rate continued to slide, down to just 1.8% which remains near historic lows. With the market remaining tight, rates have stayed relatively flat at their “new normal”. At the end of Q1 there were only three vacant office spaces in Carpinteria totaling about 8,200 SF. With such limited available inventory, there was just one new office lease during the quarter, for 3,425 SF at 1029 Cindy Ln. Again, with total industrial volume at only around 465,000 SF, the market can change quickly if a company like ProCore or Microsoft were to exit. Microsoft recently purchased some of the buildings they occupy which is a great sign for this market.

|

Industrial

Santa Barbara’s industrial sector remains stable, with a minor uptick in vacancy to start the year, rising from 0.6% in Q4 ‘18 to 0.8% in Q1 ‘19. In fact we have not seen the vacancy rate above 1% since 2014. There was just one new lease during the quarter, at 308 Palm Ave. for 3,078 SF and $2.10/SF Gross. Average asking rates have hovered between $2.38/SF Gross and $2.67/SF Gross since the beginning of 2018, and with such continued limited supply we may see actual rates continue to increase. Currently there are 10 vacancies accounting for just over 36,000 SF.

There was little change in Goleta’s industrial sector as well, with the vacancy rate increasing only slightly from 6.0% at the end of 2018 to 6.1% by the end of Q1 ‘19. That said, this is the highest vacancy rate since 7.5% back in early 2012. There were 10 new leases signed during the quarter totaling just over 65,000 SF, with an average gross achieved rate of $1.64/SF. With a healthy vacancy and limited available product, we may see little fluctuation in the lease rates through the year. Notable leases during the quarter include the recently updated buildings at 749 and 759 Ward Dr., with HERBL Inc. taking both for over 25,000 SF total.

Down in Carpinteria, the industrial vacancy rate dropped to its lowest level in a year at 1.6%. This was due to four leases accounting for approx. 23,300 SF or just more than half the amount of vacant space from the previous quarter. We do not expect much change over the next few quarters as there are only two remaining industrial vacancies in the area that total 20,900 SF of leasehold space.

Retail

The big retail news during Q1 didn’t involve a deal or a closure, but instead the long-awaited opening of a mini Target at State and La Cumbre. Despite the store’s “small-concept” footprint, the popular retailer’s arrival is a much needed shot in the arm when other big box chains (Macy’s, Sears, Kmart) have exited the market.

The volume of space available for lease has grown year over year. At the end of Q1 2018 there were 79 properties available comprising 332,057 SF. At the end of Q1 2019, inventory rose to 92 properties comprising 393,851 SF, an 18.6% increase in square footage. Notably, spaces at 901 State St. (18,357 SF | Forever 21), 710 State St. (8,800 SF | Restoration Hardware), 2605 De La Vina St. (6,620 SF | Jedlicka’s) came to market during the quarter, adding to the city’s retail vacancy.

When looking specifically at State Street, there were 32 retail storefronts between the 400 and 1300 blocks available for lease at the end of Q1, which represents a 12.9% vacancy rate. This was virtually unchanged from Q4 ‘19.

In Q1 ‘19 overall there were 12 new leases (31,047 SF) signed in Santa Barbara, an improvement from the 11 leases (18,507 SF) signed in Q1 ‘18. The average gross achieved rate rose from $3.53/SF a year ago to $3.95/SF in Q1 ‘19. In Montecito there was just one small lease for 675 SF at $7.59/SF Gross.

|

State Street Quarterly Retail Vacancy Update

Radius conducts a monthly visual inspection and research of the downtown State Street corridor (400–1300 blocks). Vacancy rates are calculated based on State Street-facing storefronts only, excluding first floor office spaces fronting State Street. Some spaces may be leased and we are not aware. Pop-up shops are included in the vacancy rate given their short term status.

Key Observations

-

-

- State-us quo. No real change on State during Q1 with the same number of spaces available for lease as in Q4 ‘18 (32), and just one more vacant storefront (23). Noticeably there were fewer Pop-Up shops, down from 7 to 3.

- Fresh faces. There were 6 new retail leases signed during the quarter totaling more than 13,428 SF: 601 State St. (House of Clues Escape Room | 4,653 SF); 1026 State St. (The Latteria | 2,628 SF); 427 State St. (Random | 2,500 SF); 1019 State St. (Turkish Coffee Lounge | 2,300 SF); 506 State St. (E-Bikery | 1,347 SF); 630 State St. (Glasshouse Patio | Size Unknown).

- Not out of the woods yet. Two larger storefronts came to market during the quarter at 901 State St. (Forever 21 | 18,537 SF) and 710 State St. (Restoration Hardware | 8,800 SF). Though these retailers still occupy their spaces, should they choose to vacate it will create two more sizable craters that need filling.

Multifamily Sales Summary

South Santa Barbara County

We continued to experience slowed multifamily sales activity during Q1 with only four sales of properties 5+ units in size, no real change from the three recorded in Q1 2018. As with all parts of the South Coast, and really most of the Central Coast, it continues to come down to supply and demand as many investors wait eagerly in the wings with very few properties available. In Isla Vista, for example, one of the most coveted sub-markets in the region, there were no sales in Q1 and just a couple of active listings at this time.

Clearly we are seeing property owners reluctant to part with lucrative assets as apartment vacancy rates remain historically low. Isla Vista, for its part, continues to be a huge draw for UCSB students and therefore for investors interested in multifamily property. In fact the demand for apartments continues at record levels throughout the Central Coast and the multifamily market should remain positive for 2019.

In Santa Barbara, for example, renters make up a majority of the population keeping vacancy rates low. The apartment vacancy rate remains around 2% on the South Coast, and has remained below 2% since 2011 (Dyer Sheehan). The City of Santa Barbara stands at 1.86%, Isla Vista at 1.82% and Goleta slightly higher at 2.06%. Carpinteria has an extremely low vacancy rate of about .09% with rents remaining stable. Contrast these figures with the reported national apartment vacancy rate of 4.8%, unchanged from Q4 2018 to Q1 2019 and buoyed by a strong economy and stable unemployment rates, and you can clearly see why the South Coast is such a favored market among investors.

Q1 Highlight Sales

- 1501 Santa Barbara St., Santa Barbara / 8 Units: $4,394,000, $549,250 PPU (1/16/19)

- 822 Olive St., Santa Barbara / 8 Units: $2,150,000, $430,000 PPU, 4.31% CAP (2/20/19)

North Santa Barbara County, San Luis Obispo County

Not much new to report in the northern part of our Central Coast region. In the Santa Maria and Lompoc areas, the demand for larger multifamily properties is as strong as ever, yet the market remains very tight with no sales of 5+ unit properties reported in Q1. In fact there is just one 12-unit building currently in escrow and only two listings of properties 5+ units in size available for sale. In San Luis Obispo County, this hot market also continues the trend of high demand and low supply. In Q1 we know of just two sales of 5+ unit properties.

Q1 Highlight Sales

- 284 N. Chorro St., San Luis Obispo / 34 Units: $9,850,000, $289,705 PPU (3/27/19)

- 3380 Bullock Ln., San Luis Obispo / 8 Units: $1,615,700, $201,963 PPU (1/25/19)

Ventura/Oxnard

It’s a similar story to the south in Ventura County with demand continuing to outweigh inventory. There were just six sales of 5+ unit properties during Q1, with just a handful of larger properties currently available. It’s no surprise given the strength of the rental market, with a county-wide vacancy rate of just 2.6% in January 2019, that the sales market remains tight as many owners see no reason to divest of their properties as long as income remains stable.

Q1 Highlight Sales

- 520 W. Channel Islands Blvd., Oxnard / 36 units: $5,600,000, $155,555 PPU (3/1/19)

- 461 W. Channel Islands Blvd., Oxnard / 12 units: $2,200,000, $183,333 PPU, 4.58% CAP (1/18/19)

-

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …