|

Message From The Radius Team:

This is a trying time on all fronts. Every person around the world is impacted by the spread of the novel coronavirus, and though it may feel a little shallow to consider the effects of COVID-19 on the commercial real estate industry, our job as professionals is to ensure our clients are fully prepared to move forward with recovery. We will get through this.

Our generation (let’s face it, EVERYONE is in this together) has certainly seen tragedy and hard times. The events of 9-11 and the Great Recession come to mind. This is different. For most of us it feels like the world has ground to a complete halt, with the exception of our essential workers and frontline healthcare heroes who thankfully are trudging along because they must.

But if you look closely, beyond our empty streets and 2-D television screens, you’ll see the heart of our economy still beats. In fact there are workers out there every day doing what they can to keep the economy moving. Restaurants working behind closed doors have evolved into small grocery co-ops and delivery services. Companies are actively seeking out warehouse and industrial space to store goods that are being ordered online and shipped direct to consumer. Others are transitioning their manufacturing to meet immediate needs big and small, everything from creating test kits to sewing masks. Yes, this is our economy for now. That will change in time.

We have talked with many of you over the past few weeks and will continue to reach out. One common question we’re hearing right now, from landlords and tenants, buyers and sellers, is “What should I do?” Because we are in unchartered territory, there are many underlying considerations and certainly a wealth of sometimes contradictory opinions. But where we are trying to focus the conversation is around communication.

The fact is we are living in a fluid situation, and now more than ever we need to talk. Perhaps nowhere is that more important than between landlords and tenants. We would advise clients to be honest and open in these conversations, and to seek flexibility wherever possible. For example, while there are restrictions in place for certain types of evictions, those will not always be there and landlords will look to be made whole. If you are a tenant who has been truly impacted by current events, be prepared to open your books to your landlord. For the owners, we would advise trying to be creative, where possible, with agreements that give some respite now but with the understanding that it is recouped in the long term, either through an extended lease or through a payment plan, for example.

On the sales side we believe there could be opportunities for buyers coming up depending on their sources of income. Lending is still happening, but be prepared for hiccups that may come along depending on a lender’s level of comfort with this new economy. Sellers need to consider whether now is truly the best time to go to market, and if they do they should be prepared for deals to take longer.

And on our end, know that your commercial real estate professional will be there to guide you through the process. Almost daily we receive new information on changing regulations, guidelines and best practices in transacting commercial real estate. There has never been a more challenging time to consider going it alone, so we strongly encourage you to pick up the phone. The Radius Team will work with you to find answers, solutions and success.

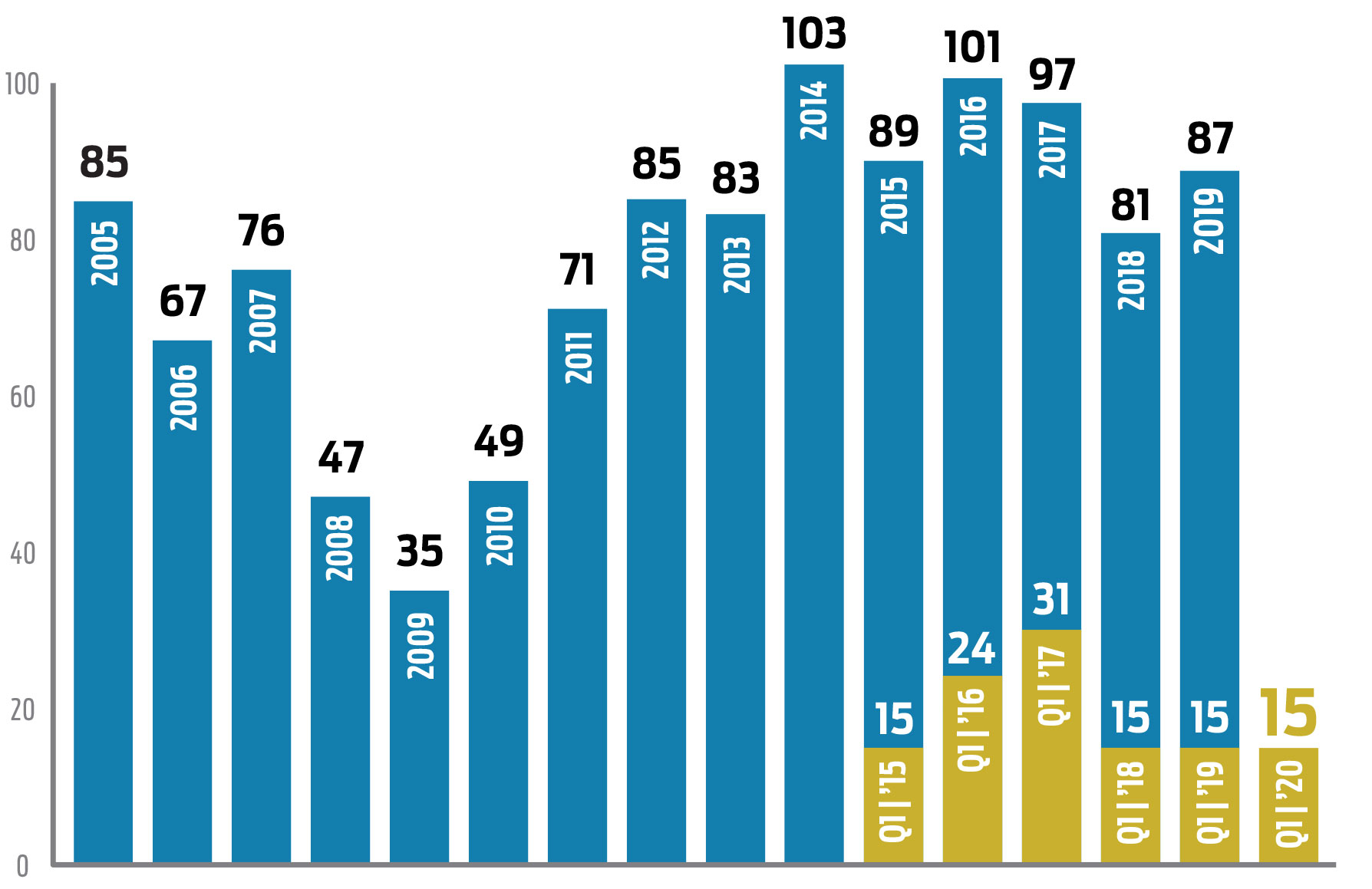

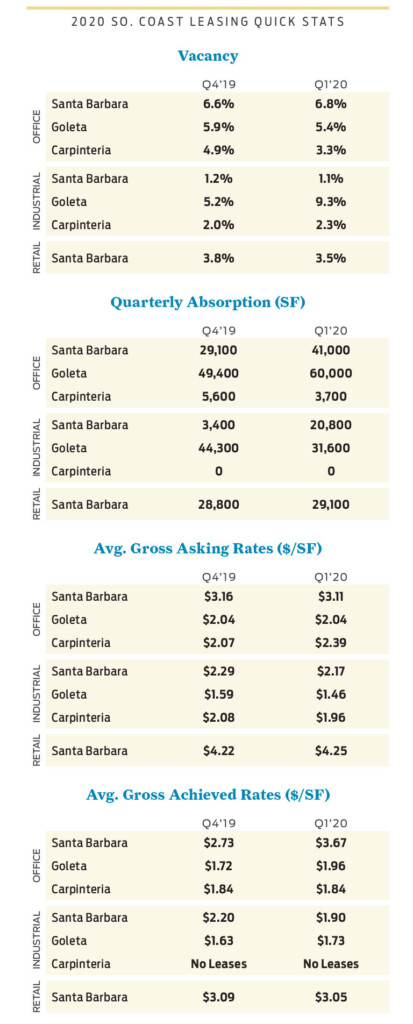

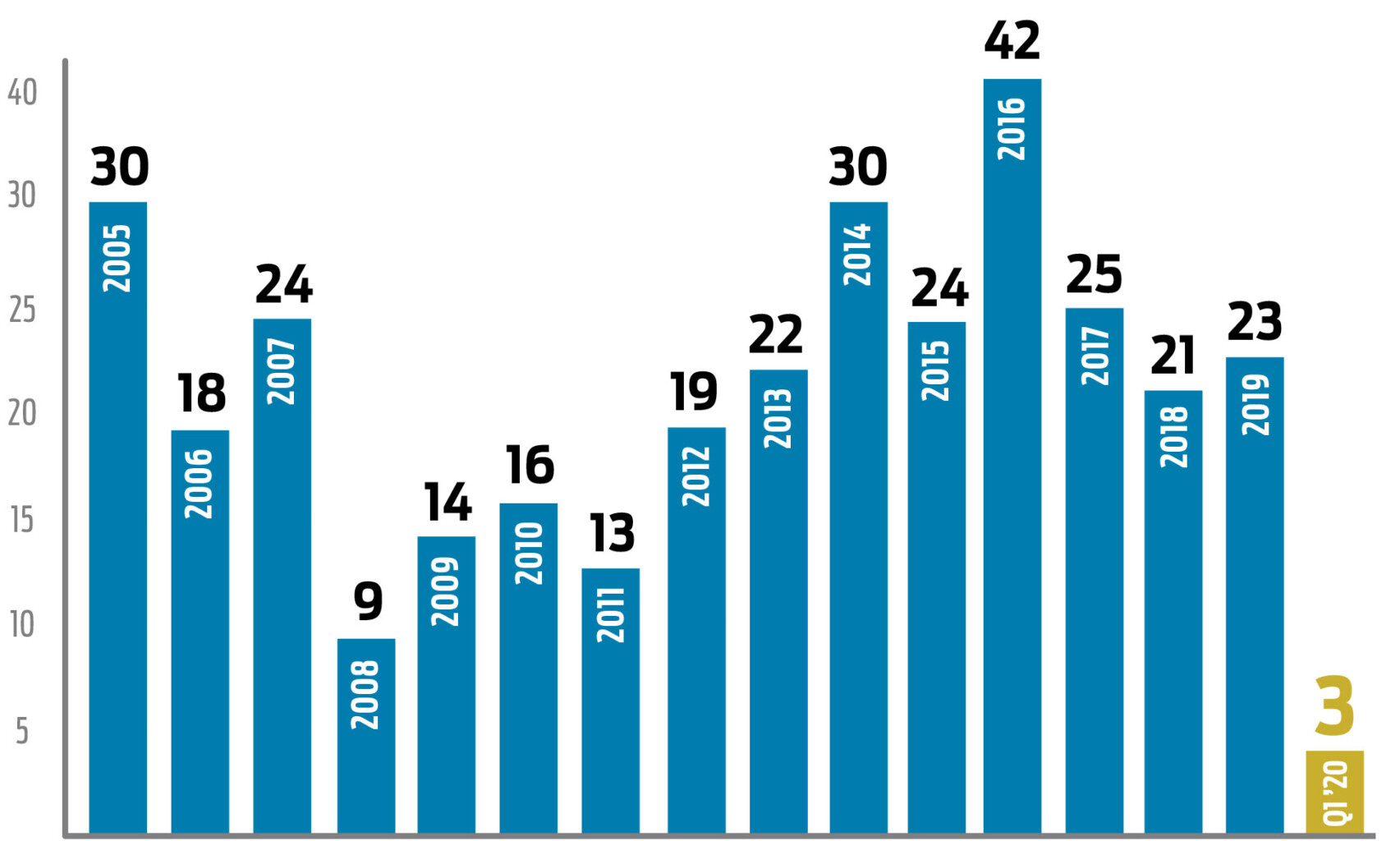

Q1 2020 Commercial Sales Summary: What a difference a quarter makesThe recent “Corona Crisis” has sent everyone into lockdown, thrown all financial markets into a tailspin and brought commercial real estate activity to a crawl.Since none of us have lived through a crisis that included both a pandemic and stock market meltdown, it is difficult if not impossible to predict the direction of the market. We do think it is safe to say that most investors will be cautious observers for the immediate future, watching to see how and when we recover from these setbacks. Financing and available credit will also be key to restoring some stability in the market for both investors and owner-users. It seems like just yesterday when we reported year-end statistics and status for 2019, noting a market that was humming along with some pretty stable numbers for sales and increasing totals in dollar volume. While the number of deals during the first quarter of 2020 are somewhat normal, boy how times have changed. From January through March we did see 15 commercial sales on the South Coast, matching the first quarter totals in both 2019 and 2018. What has changed dramatically is dollar volume. This year we slipped down to just $39.2MM, or roughly 38% of Q1 2019 ($104MM), and about 19% of Q4 2019 ($210.6MM). Difficult to say if any trend is to be deduced given current circumstances, but again all eyes will be on the coming several quarters. The largest sale during the first quarter was an office building at 1145 Eugenia Pl. in Carpinteria. This 27,772sf building traded for $9MM, which represents a 6% cap if the building was fully leased (9,000sf is vacant). Other notable sales included a 7,000sf office building with two apartment units at 115 E. Micheltorena St.—previously home to the accounting firm MacFarlane Faletti & Co.—which sold for $5.6MM to an owner-occupant; and the two-story, 13,241sf retail building at 524 State Street—the former Scientology building—which sold for $5.7MM. The buyer in that one was a group of investors with plans to transform the property into a boutique hotel. By the numbers, during the quarter there were eight (8) office sales, two (2) industrial sales, one (1) land sale, and four (4) retail sales. Once again, owner-users outnumbered investors 10-to-5. Needless to say, most of these transactions were in advanced stages of escrow before the Corona Crisis. For now, we are all paying special attention to the progress of the pandemic for our own health and well-being. As business people, we are also closely watching the effects of the federal government’s interventions to see if that will help soften the blow and get everyone back on their economic feet in the near future. As history has shown, the South Coast has tended to fair better than other markets during slowdowns. Only time will tell.

|

|

Perhaps the biggest and most obvious question mark is the retail sector. Our local retailers have had to endure many challenges over the past several years in the form of the fires and mudslides that devastated our communities as well as the increased popularity of online shopping, and current circumstances have dealt yet another gut-punch from which to find a way to recover. We have discussed at length the State Street conundrum in particular in past reports and recent events will likely put our struggling “main drag” under even more immense pressure and scrutiny.

But the South Coast market’s traditional lack of new supply of office, industrial and retail space may turn out to be somewhat of a saving grace, allowing us to maneuver these uncertain times in better shape than other markets.

During these unprecedented times communication between landlords and existing tenants will undoubtedly be paramount. Landlords will need to understand that tenants’ monthly payment obligations may need to be temporarily modified in order to keep the tenant’s business viable. At the same time tenants will need to understand that landlords have (at minimum) fixed building expenses such as mortgage, taxes, insurance, maintenance, etc. that need to be met. The bottom line is all parties are taking it on the chin right now, so we all need to be in each other’s corner if we’re going to make it through these rounds.

Today we are in unchartered territory, understatement of the year. But by the end of the second quarter we should start to see a clearer picture of the fallout of this crisis as well as the path forward.

|

Q1 2020 Multifamily Investments Summary:

South Santa Barbara County

The year started with multifamily sales activity in the local market continuing as previous quarters, but the first quarter of 2020 ended on uncertain footing along with all financial markets as the COVID-19 pandemic emerged.

While the stock market and and the commercial real estate industry are getting hit substantially as the financial impacts of the virus are difficult to quantify, multifamily real estate still remains the safest of investment real estate property types due to the constant need for housing, no matter the circumstances. With other commercial sectors like retail obviously getting hit harder and with instability in equity markets, multifamily may strengthen as investors seek stability. Furthermore, our local Santa Barbara communities, a long-time safe haven for investors, has shown resistance to the pandemic due to its geography, roughly 100 miles from the nearest metropolitan area, and lower density than other areas in California.

Before the pandemic gathered steam, very little inventory had traded in our region. As usual, a high number of investors continued to be in the hunt for opportunties, but most properties ended up trading off market. With this low inventory, there were really only three highlight sales in the County, one in Isla Vista, one in Santa Barbara and one in Santa Maria. Again, none of these assets were broadly marketed. The largest of these was the sale of the Breakpointe and Coronado complexes, two student housing assets in Isla Vista totaling 149 units. The deal closed at $73,700,000 or roughly $495,000/unit, despite trading just three years ago for roughly 70% of that price. The new owner was able to capitalize on a minor rehabilitation of the assets, low interest rates and pent-up investor demand for student housing, quietly marketing the offering and ultimately selling on a by-the-bed basis. Selling student housing assets by the bed has helped owners increase their sale price per unit by maximizing revenue for skilled operators who can utilize this leasing strategy. Interestingly enough the asset sold just before the closure of the UCSB campus. Even though the school remains shut down, rent collections are still hovering around 80 – 90 percent and pre-leasing is still occurring. The major question remains whether UCSB will open on schedule for the fall quarter. If it doesn’t, rent collections may drop next year and landlords could have a harder time enforcing leases.

The other two highlight sales were in the city of Santa Barbara and Santa Maria, both being sizeable off-market transactions. An 18-unit building at 401 W. Los Olivos St., Santa Barbara near Cottage Hospital and consisting of all studio units closed for $4.7 million. Both the buyer and seller had new hurdles to climb with fresh state and local rent legislation—including the AB1482 rent cap bill and the City of Santa Barbara’s mandatory 1 year lease offer ordinance—creating additional paperwork. With a building such as this with below market rents, the buyers were still able to achieve attractive financing by showing upside over a longer period of time, even though the new rent cap of 5% + CPI staggers those returns over a longer period. Still, month-to-month tenancy helps as there is a naturally higher rate of turnover, allowing the new owner to more quickly achieve market rents.

Meanwhile in the North County, a property at 317 – 323 N. Western Ave. sold for $5.5 million. This was a heavy value-add deal selling to a Los Angeles based investor with a concentration of assets in Santa Maria. The price per unit was $137,500, below average for Santa Maria. The next largest deal occurring in Santa Maria was at 826 W. Cook St., a 16-unit asset in a great location close to all the preferred amenities in the city. That building sold for $2.5 million or $156,200-per-door at an approximate 5.6% cap rate.

Ventura

Ventura experienced very low transaction volume during the first quarter with just two smaller assets selling. One was an 8-unit building at 6329 Whipporwill St. in Ventura. The other was located at 1829 E. Ocean Ave. which consisted of cottage-style units. There was also one 12-unit asset in Oxnard which came to market and quickly went into escrow.

Still, the Ventura markets continue to be in high demand by investors, from Camarillo through Ventura and into Ojai. There are a few sizeable off-market deals in escrow and one or two assets possibly coming online in the coming months.

San Luis Obispo

San Luis Obispo did not record any sizeable transactions in Q1, similar to Ventura. There is one 13-unit student housing asset adjacent to the Cal Poly campus at 1238 E. Foothill Rd. that has seen multiple escrows and is back in escrow again, possibly closing in the next two months.

According to several student housing owners, pre-leasing for the fall was slightly stronger this year than last and collections have been at approximately 80 – 90 percent despite COVID-19.

Lending Update

Clearly COVID- 19 has caused much disturbance to the real estate markets as tenants have borne the direct impact. The ability to earn revenue and pay rent ultimately will find its way to landlords. While this is a massive problem in retail and office real estate, tenants are receiving help paying their rent from the unprecedented government stimulus package and broadened unemployment compensation. Lenders are mostly pulling back on lending to other property types but many local and national banks are still bullish on multifamily, as they should be, since we can see that the fundamentals are still strong.

Nevertheless, risk is still increasingly prevalent as, over the short term, unemployment will hamper asking and achieved rents from apartment tenants. To compensate for this additional risk, many lenders are increasing their debt service coverage ratios and although the federal funds rate is 0%, interest rates are flat to possibly increasing slightly, and appraisals are coming in more conservative as well.

Still, there is money out there for multifamily and relationship lending is the name of the game. Local banks want to keep their relationship clients happy and are doing their best to extend credit to strong clients at numbers that aren’t too far off from before the pandemic.

Recent News

Pacific Coast Business Times: CRE: American Riviera Bank buys Ventura branch office

Most banks lease their local branches and standard offices, but American Riviera Bank decided to go against the grain, announcing that …

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …