Please download the complete Q1 2021 market report here or contact your Radius broker for more information.

|

Q1 2021 Commercial Sales Summary: Momentum slows in Q1

Plus lack of inventory has market doing double-take with repeat sales

At the end of the first quarter last year, at a time when the new Covid scare was fresh in everyone’s mind, no one in our industry had any idea what direction the market was headed. Many feared a major market tumble the likes we hadn’t seen for a decade. Fast forward to Q1 2021 and the commercial sales market is in a much different place than most would have expected.

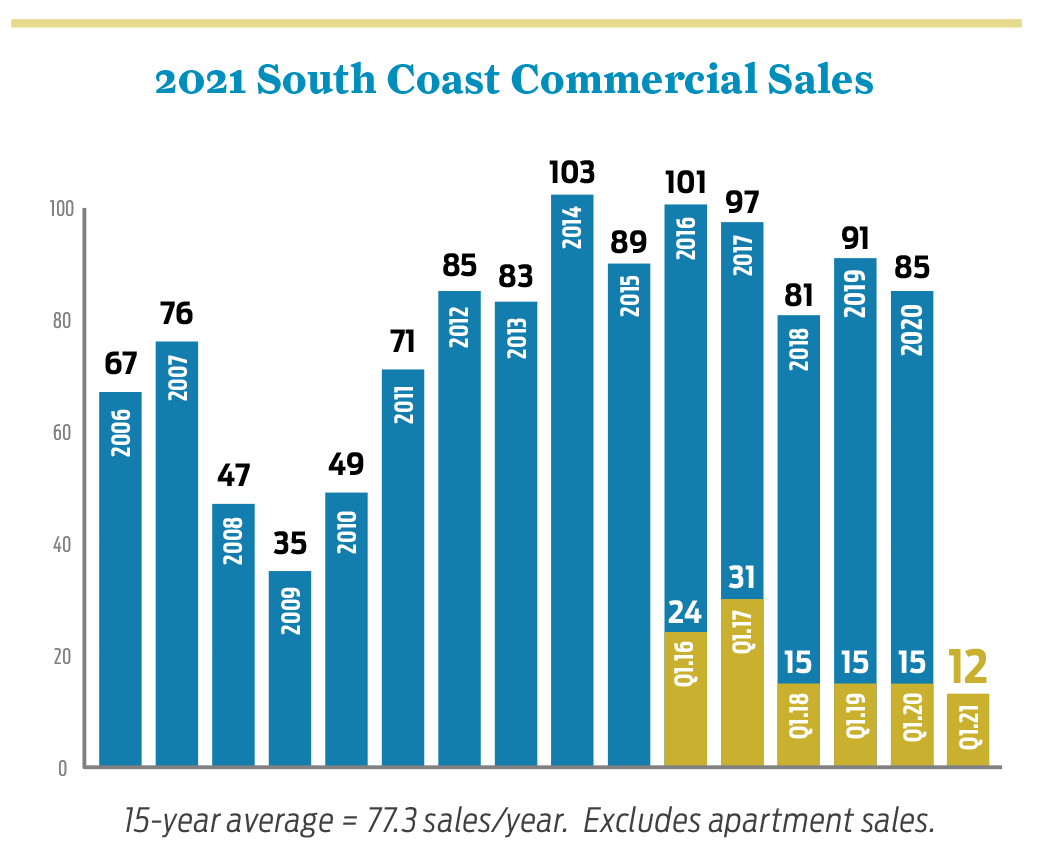

In fact, last year actually ended on a strong note with 29 sales in Q4 alone and a total of 85 for the year, just below 2019’s 91 and higher than 2018’s 81. Although that momentum slowed a bit in the beginning of 2021, there are still some interesting things to note. For one, the first quarter 2021 was almost exactly on pace with Q1 last year, seeing a total of 12 commercial sales (15 in Q1 2020) and a volume of $41.4MM ($39.2MM in Q1 2020).

Secondly, we’ve experienced a case of “sales déjà vu”. Essentially we find ourselves with a somewhat surprising lack of inventory which became even more evident when we saw two properties (225 State St. & 212. W. Figueroa St.) both sell during Q1 for the second time in less than a year, and both for more money! It is safe to say this same lack of inventory has pushed higher prices to the extent that we’ve seen a jump in average price/SF from $424/SF for Q4 2020 to $535/SF for Q1 2021.

Another interesting trend we’ve been following over the past few years has been the ratio of owner-users to investors. Q1 was 50/50 with six (6) owner-user and six (6) investor sales. And certainly another trend line is that of those six investor sales, five (5) were 1031 Exchange driven.

Breaking it down by sector, office properties led the charge with five (5) sales for the quarter, followed by industrial with three (3), retail with two (2), one (1) healthcare and one (1) land sale. Interestingly, the off-market sale of a 155-bed convalescent home at 160 S. Patterson Ave. in Goleta was the highest price sale of the quarter at $14.4MM.

So what lies ahead? With inventory down and prices going up, expect to see an increase in inventory from owners trying to capitalize on this trend. However, don’t expect to see meaningful discounts in pricing any time soon as long as real estate remains a darling to investors.

While this should bode well for sales numbers, we are still seeing a continuing move to quality and stable investments by investors. Again, Santa Barbara is one of those markets where “investment” is a relative word when you see the fever pitch of single family home sales. They don’t generate any income, but have certainly appreciated over the past year.

Q1 2021 Leasing Summary

Office

Santa Barbara’s office vacancy rate notably jumped from 8.1% in Q4 2020 to 10.0% in Q1 2021. While this rise continues a trend over the past few years, the numbers can be a bit misleading. Earlier this year the owners of the former Macy’s building on State Street made the bold decision to market the space as 100% office use. While we believe the ground floor will remain retail, the 2nd and 3rd floors, comprising ±87,500 square feet, will become office. A shift of this magnitude alone was enough to increase the office vacancy rate by 19%. We’ll certainly be keeping an eye on this property.

Overall, the first quarter was very active in Santa Barbara with 23 signed leases. The largest being Keller Williams moving from 1435 Anacapa St. to 1505 Chapala St. This was followed by Flueid Software leasing approx. 6,892 square feet of exceptional space on top of Carrillo Hill at 800 Miramonte Dr. Over the last six months, high end office spaces have seen significantly more activity than B and C quality spaces. Indeed we have watched companies that thrived during the pandemic ‘level-up’.

|

Meanwhile in Goleta, office leasing in Q1 was steady with only seven (7) new leases totaling about 70,000 SF to report, the largest of which was the 38,401 SF former LogMeIn building at 7416 Hollister Ave. which leased to Asylum Research Corp. for $2.11/SF Gross. The market vacancy rate dropped slightly from 7.1% in Q4 2020 to 6.6% in Q1 2021. Asking rates for Goleta also went down from $2.13/SF to $2.00/SF Gross, while the average gross achieved rate for the quarter was $2.06/SF. We have seen an increase in leasing activity and expect the vacancy rate to lower even more as some of the larger vacancies begin to fill up.

While vacancy across all office submarkets appeared to peak in Q4 2020, like most areas of our market in Q1 2021 Carpinteria’s vacancy rate trimmed down from 6.6% to 4.0%. The largest remaining vacancy is the ±8,896 SF sublease at 6398 Cindy Ln. It will also be interesting to see what happens with the Lagunitas Campus (entitled ±80,000 SF office building). Many thought ProCore would eventually sign a lease on the site, kickstarting the project’s construction. However, the company vacated a few spaces in 2020 and their meteoric rise in the Carpinteria office market seems to have slowed.

Industrial

Santa Barbara’s industrial sector has remained level throughout the last 12 months, with only a slim 0.2% percentage point increase in the vacancy rate to 1.3% in Q1 2021. Santa Barbara did see more leasing activity than in Carpinteria and Goleta with four perfected leases totaling ±18,739 SF during the quarter. It is interesting to note that based on where certain industrial buildings may be located, we are seeing a higher range in achieved lease rates. For instance, since the beginning of the year the lowest lease rate was at 1 S. Calle Cesar Chavez at $1.01/SF Gross. Compare this with another achieved rate for a very similar building at 208 Gray Ave. which signed for $3.18/SF Gross. Furthermore, when comparing quarters, we saw the average gross achieved rate drop from $2.99/SF in Q4 2020 to $1.92/SF in Q1 2021, a difference of $1.07/SF in the same asset class in one quarter. This dynamic is exaggerated with the consistently low vacancies in Santa Barbara, as well as a widening in the locations where these highly sought after buildings may be found.

Meanwhile in Goleta, the industrial vacancy rate has consistently fallen since Q1 2020 when it peaked at 9.3%, now 6.4% in Q1 2021. Since Q4 2020 there have only been three new leases totaling

±7,864 SF. The largest was at 289 Coromar Dr. (±4,050 SF). The achieved lease rate remained relatively static from Q1 2020 at $1.73/SF, down slightly to $1.71/SF Gross in Q1 2021. Currently we

are seeing a good deal of activity in the Goleta industrial market and we expect vacancy to drop over the remainder of the year.

Finally in Carpinteria, industrial leasing activity was slow going throughout Q1 2020 with one lease perfected at 1030 Cindy Ln., Ste. A (±4,350 SF). There were a number of industrial leases that

have been extended. One to note was the extension with Procore for 28,800 SF at 6385 Cindy Ln., Building C. Still, Procore has ±14,000 SF of it on the market for sublease. The Carpinteria industrial vacancy rate has seen the largest increase in all three submarkets since Q1 2020, climbing from 2.3% to 6.4% in Q1 2021.

Santa Barbara Retail

Not completely unexpected, Q1 retail leasing in Santa Barbara was fairly uneventful. There were a total of 12 new leases totaling approximately 19,000 SF of newly leased space. These spaces ranged in size from 500 SF to 5,740 SF. The two most notable leases were Silver Air’s 5,740 SF lease of the former Enterprise Fish Company building at 225 State St. (yet another example of an office tenant leasing what in the past had been a retail space) and a spirits bar concept’s lease of 3,500 SF at 700 State St.

On the vacancy front, the vacancy rate notably clicked down from 5.0% at the end of 2020 to 4.3% to end Q1 2021. It must be clarified this is largely due to the reclassification of a big chunk (about 87,500 SF) of the former Macy’s building located at 701 State St. in the Paseo Nuevo from retail to office use. We will certainly be keeping an eye on this property as ownership has chosen to market the upstairs portions of the property at the corner of State and Ortega Streets as office. Now known as “The Ortega Building”, it has been on the market for about four years now. No doubt the Lessor would still welcome a deal(s) for a larger retailer(s), but in a market where such deals are few, casting an “office net” in the hopes of capturing a tenant similar to Amazon at the former Saks building on State Street is understandable and a “sign of the times.”

Asking rates for Santa Barbara retail have remained constant at approximately $4.00/SF Gross Equivalent (Base Rent + NNN) while Achieved Rates clicked up from $3.31/SF to $4.01/SF Gross Equivalent.

|

Q1 2021 Multifamily Investments Summary

South Santa Barbara County

Three months in to the new year and we are still seeing an adjustment in Santa Barbara County multifamily sales due to the pandemic. Although the market is strong, inventory remains low, generating multiple offers on many listings. Demand for apartments is still high even with the delivery of new development projects.

A total of 15 investment properties sold in Santa Barbara South County in Q1 of 2021. There were five (5) transactions in the 5+ unit range and seven (7) transactions in the 2-4 unit range in the City of Santa Barbara. Montecito added two (2) sales of 2-4 unit properties, while Isla Vista finished with just one (1) transaction of 4 units. Again, we are seeing multiple offers on many listings as inventory remains low in the market.

The largest transaction during the quarter was at 160 Camino De Vida in Santa Barbara. This 12-unit building sold for $4.21MM ($350,000/unit) at a 3.39% cap rate. Additionally, an 11 unit building at 304 W. Cota St. garnered just over $3.5MM at $319,091/unit, representing the largest asset sold in the downtown area during the quarter. In the 5+ unit range the average price per unit was $389,652. In the 2–4-unit range there were seven (7) significant transactions in Q1. The highest price per unit achieved was at 836 W. Arrellaga St. ($692,000). This 2-unit property traded for $1,385,000. The average price per unit for properties in the 2–4 unit range was $576,774. Just one property traded in Isla Vista during Q1, located at 6509 Pardall Rd. This 4-unit building sold for $2.6MM at a cap rate of 4.65%. Meanwhile in Montecito, a 4-unit building at 66 Eucalyptus Ln. sold for $7MM at $1,750,000 per unit. Another notable sale was a 2-unit building in Montecito that traded for over $2.8MM with price per unit just over $1.4MM.

North Santa Barbara County

Moving into North County, the tale of scarcity in our region continues as we did not see any transactions involving 5+ unit properties during the first quarter. That said, a 12-unit building did come to market just this quarter at 221 N St., Lompoc, priced at $2,150,000 at a 4.77% cap rate and $179,167/unit.

W. Ventura County

Down south to W. Ventura County, there were four (4) transactions of 5+ units during the quarter. The largest being a 50-unit property at 850 Warwick Ave. in Thousand Oaks. This property sold for $16.1MM at $322,000/unit and a cap rate of 4.36%. Oxnard and Camarillo each had just one (1) sale in Q1. In Oxnard a 5-unit building located at 2230 Saviers Rd., sold for $1,080,000 at $216,000/unit, while in Camarillo at 1720 Ventura Blvd., an 8-unit building sold for $2,050,000 at $256,250/unit. The average price per unit in W. Ventura County during Q1 was $312,162.

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …