Summary of market insights and analysis from Q2 2019 South Coast commercial sales and leasing activity: Download the complete report here or contact your Radius broker for more information.

|

Commercial Sales Summary: Steady-as-she-goes

With the 2nd Quarter of 2019 in our rear view, the South Coast market seems to be following suit similar to Q1 2019 and the first two quarters of 2018. Sales closed during Q2 2019 totaled 15, the lowest quarterly figure since Q1 2018. This brings the first half of 2019 to a total of 30 commercial sales, just one more transaction than the first half of 2018.

The local market seems to be trending slightly below the 15 year average of 75.4 sales per year. However, in years past sales have tended to increase during the last two quarters so we should expect to end the year close to our annual average. Still, South Coast annual sales have in effect been on the decline since 2016 which saw a near market high of 101 sales.

Focusing on commercial sales volume, Q2 2019 amounted to $69.2 Million versus $103.7 Million in Q1 2019, for a total of $172.9 Million during the first half of the year. This is higher than the $103 Million in the first half of 2018 yet lower than the $203.5 Million in the first half of 2017.

Digging deeper into Q2 2019 figures, the majority of sales (5 total or 33%) involved office properties, with sales volume and square footage for this category significantly outnumbering the other asset types at $50.2 Million (72% of total Q2 sales volume) and roughly 131,000 SF (75% of total Q2 square footage).

For Q2 2019 sales we also saw a near-even mix of investors and owner-users, with 8 properties (53%) purchased by investors and 7 properties (47%) purchased by owner-users. Owner-users are continuing to take advantage of historically low SBA rates and comprise a healthy percentage of the buyer pool.

|

Notable Sales

420 S. Fairview Ave., Goleta

In the largest commercial sale of the quarter, this Goleta office property traded at over $22.8 Million to Yardi Systems, the existing tenant of the 72,200 SF building.

834 State St., Santa Barbara

In another “tenant purchases building” deal, this 23,373 SF office building was purchased by Bank of America for $7,100,000 ($304/SF) at an extremely low CAP Rate of 3.05% due to Bank of America possessing a long-term, under-market lease rate.

Predictions

Now eclipsing a 10-year bull market, we are entering uncharted waters. With extremely low CAP rates, recent Fed interest rate cuts and the concern of a real estate bubble, it is hard to predict when this real estate wave will end. Our cautious advice, if you want to sell in the next 5 years, now may be a good time to do so. If you like your current investments then hold and refinance. If you are looking to buy, be prudent. Contact your broker for a private consultation.

|

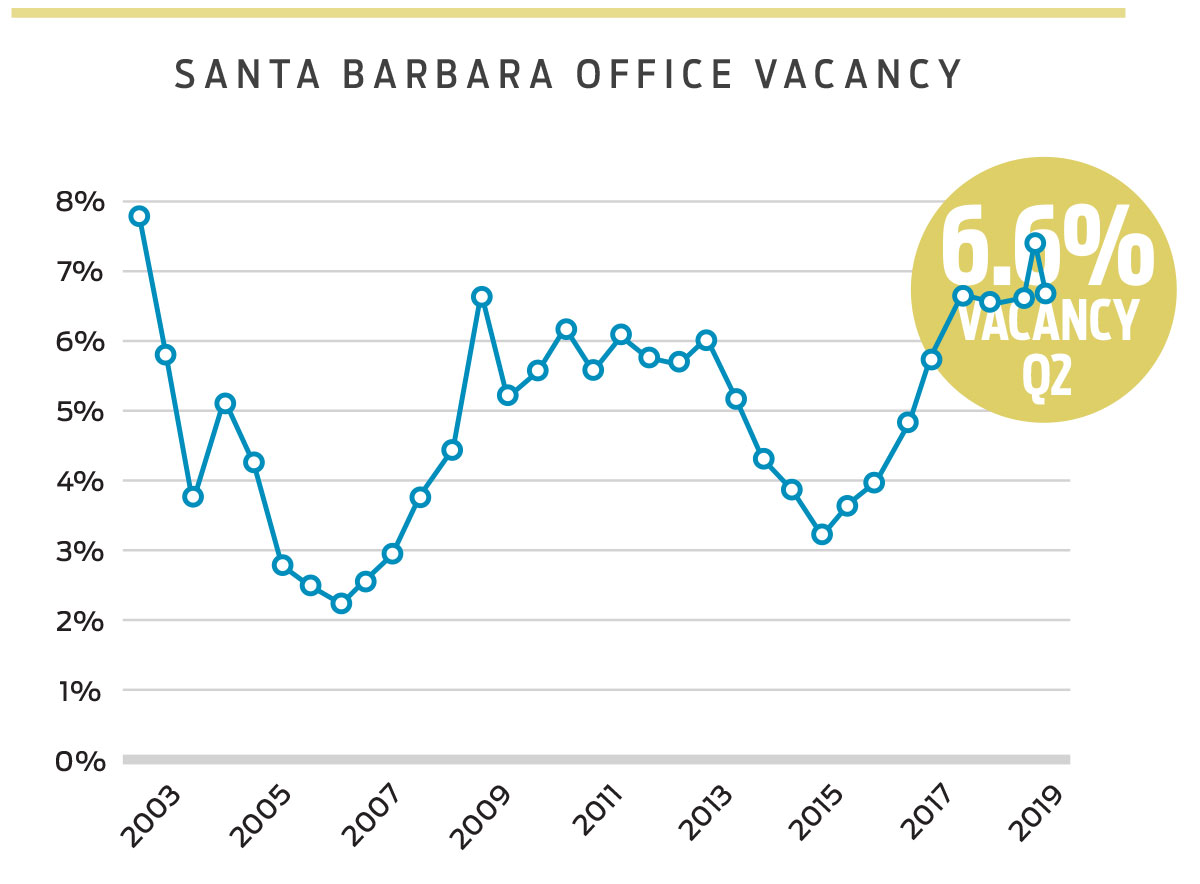

Leasing Summary: Santa Barbara Office vacancy rate still high at 6.6%; Goleta dips to 5.2%

Office

The office vacancy rate in Santa Barbara commercial real estate decreased from 7.4% in Q1’19 to 6.6% in Q2’19, but still remains at the higher end of what we’ve seen since 2003. Also of note, Santa Barbara vacancy rates have historically been lower than Goleta but this has not been the case over the past few quarters as Goleta has seen its vacancy drop to the 5.0–5.5% range.

The two largest new leases of the quarter involved 27 E. Cota St. (8,000 SF | Umbra Lab LLC) and 12 E. Carrillo St. (5,708 SF | PayJunction). A 5,082 SF space at 3820 State St. had been vacant for a considerable amount of time and finally leased in May.

The average gross asking rate dropped slightly to $3.16/SF, while the average gross achieved rate rose from $3.10/SF to $3.18/SF. There were 30 new leases signed during the quarter for a total of 65,868 SF.

Of the approx. 115 current office vacancies in Santa Barbara, roughly 70% are below 3,000 SF in size. The largest vacancy is a 26,339 SF space for sublease at 402 E. Gutierrez St., the former home of Rightscale.

We expect vacancy to remain stable throughout 2019 and look for rates to rise in the near future.

Meanwhile in Goleta, the office vacancy rate ticked down further from 5.5% during Q2’18 to 5.2% in Q2’19. Goleta office vacancy rates have not been in this range since 2007. There were 12 new leases signed during the quarter for a total of 106,675 SF, with the largest being a nearly 40,000 SF lease extension at 6550 Hollister Ave.

Parking has become a bigger issue in the Goleta office market as tech tenants are employing more employees per square foot than we have ever seen. Many Goleta office buildings are only parked 3 parking spaces per 1,000 square feet of building space while some tenants might have 6 employees per 1,000 square feet. Carpinteria is experiencing a similar issue, while Downtown Santa Barbara is best equipped to handle tech tenants based upon its various parking options.

Down in Carpinteria the office market continues to see very little change with historically low vacancy rates. The single 1,200 SF lease signed during the quarter and two vacant units yield a Q2 vacancy rate of just 1.5%.

The growth of Procore and Microsoft has transformed the office market with numerous companies gaining confidence to operate out of this beach town with less than 20,000 residents. With the combination of thriving tech environment and well-funded cannabis companies, we will likely see a continuation of the low vacancy rates in 2019.

|

Industrial

With continued lack of industrial inventory across the South Coast, vacancy remained stable in Q2 with Santa Barbara at 1%, up slightly from .8% in Q1, and Goleta at 5.4%, down from 6.1%. Carpinteria did see a markedly but not surprising decrease in vacancy, dropping from 1.6% to .1% due to just two new leases signed during the quarter at 570 Linden Ave. (20,000 SF; occupied for years by Tyco but now leased to a new-to-market tenant) and 1132 Mark Ave. (11,259 SF; Gigavac). As we know the vacancy rate can swing widely in Carpinteria given the submarket’s limited inventory.

The largest transaction in Santa Barbara was a sublease of just 3,500 SF at 517 Richardson Ave., while there were only five new leases signed during the quarter totaling 10,957 SF. There remains very little available inventory in Santa Barbara, with just over 48,000 SF comprising 10 spaces.

The majority of the 223,000 square feet vacant industrial space in Goleta (85%) remains in the 10,000 SF+ range with smaller industrial spaces simply hard to come by. It’s worth noting that the new cannabis sub-sector continues to impact industrial activity with 25,807 SF leased by Herbl at 839 Ward Dr. (the largest new industrial lease of the quarter in Goleta) bringing that tenant’s total to over 50,000 SF between three buildings.

Average gross asking rates in Santa Barbara have remained relatively flat over the past four quarters, up from $2.42/SF in Q1 to $2.52/SF in Q2. Carpinteria has seen a trend of gradual rate increases and finally cleared the $2.00 mark in Q2, at $2.03/SF gross asking.

Notably, after years of increasing rents, executed lease rates were down a bit off of asking rents signaling more of an equal tenant/landlord advantage.

While the forecast remains stable with little movement in rates and vacancy levels in the foreseeable future, we are expecting to see new buildings constructed at the Cabrillo Business Park that will test the market for new, premium industrial space for lease.

Retail

There were just 16 new retail leases signed in Santa Barbara during the quarter, the largest in May at 634 State St. when M. Special Brew Co. leased the 4,000 sq. ft. space vacated by Tonic Nightclub on lower State Street. The vacancy rate dropped nominally from 3.8% in Q1 to 3.7% in Q2, but it could have easily swung the other way had a handful of tenants in the downtown and Funk Zone areas decided to not re-up. This included lease renewals at 701 State St. (Restoration Hardware | 8,800 SF), 110 Anacapa St. (Hazard’s Cyclesport | 5,000 SF) and 4 E. Yanonali St. (The Blue Door | 4,824 SF).

Breweries continue to target Santa Barbara as a great location to showcase their product. In addition to M. Special Brew’s forthcoming opening on State Street, adding a new food concept to boot, Rincon Brewery, which has locations in Ventura and Carpinteria, signed a lease at 205 Santa Barbara St. in June and will open their third Central Coast location after the permitting and approval process. Meanwhile, Montecito continues to prosper with new developments and stores opening, including Santa Barbara Running and Lululemon Pop Up (the company’s new seasonal store concept) absorbing two vacant spaces at 1046 Coast Village Rd., and Sushi Bar opening in the Montecito Inn.

Year over year the 3.7% retail vacancy rate is the same as it was in Q2’18. Although State Street and other pockets of the city have experienced noticeable vacancy, overall retail landlords achieved $3.18/SF Gross rates for the quarter, which is $0.30/SF higher than Q2’18.

|

State Street Quarterly Retail Vacancy Update

Radius conducts a monthly visual inspection and research of the downtown State Street corridor (400–1300 blocks). Vacancy rates are calculated based on State Street-facing storefronts only, excluding first floor office spaces fronting State Street. Some spaces may be leased and we are not aware. Pop-up shops are included in the vacancy rate given their short term status.

Key Observations

-

-

- State-us quo continues. There was virtually no change on State Street during Q2 with 31 available storefronts for lease and 22 of those being vacant, which equates to a 8.84% perceived vacancy rate.

- New leases. There were 5 new retail leases signed during the quarter totaling 12,649 SF: 634 State St. (M. Special Brew Co. | 4,000 SF); 1220 State St. (Wendy Foster Inc. | 2,800 SF); 1345 State St. (Ebikezzz | 2,400 SF); 718 State St. (Apna Indian Cuisine | 1,964 SF); and 1213 State St. (Taqueria SB | 1,485 SF). Notably, Restoration Hardware renewed their 8,800 SF space at 710 State St.

- New vacancies. Three storefronts came to market during the quarter at 530 State St. (Samy’s Camera | 11,450 SF), 1021 State St. (Rocket Fizz | 2,500 SF) and 619 State St. (Beads of the Earth | 1,935 SF).

-

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …