Please download the complete Q2 2020 market report here or contact your Radius broker for more information.

|

Q2 2020 Commercial Sales Summary: Corona Crisis Curbs Enthusiasm

“Steady as she goes” downshifts to “Proceed with caution” for investors, owner-users & lenders

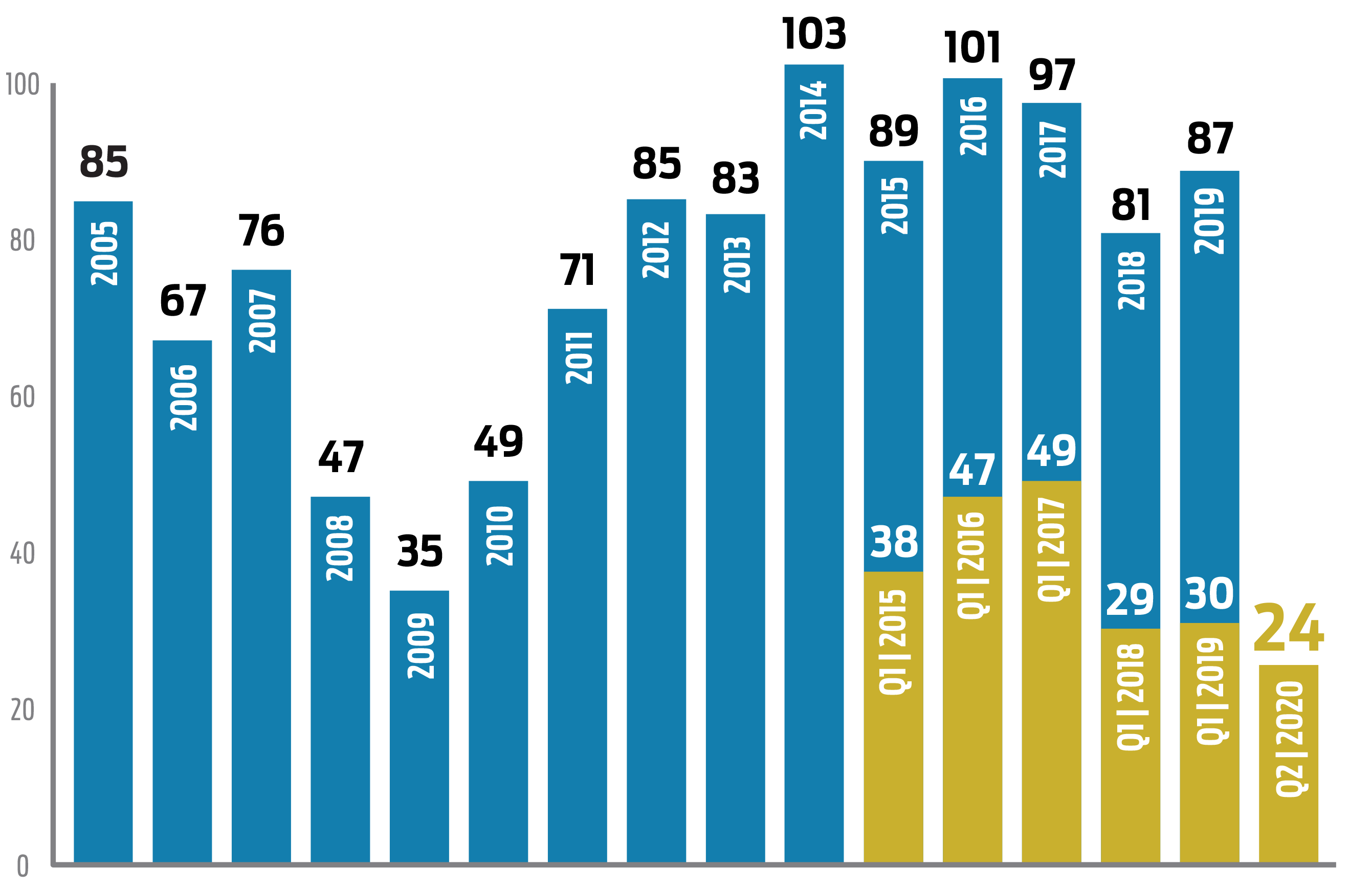

To absolutely no one’s great surprise, when you shut down an entire economy, financial activity in all areas of commerce slows down DRAMATICALLY. After living under unprecedented conditions during the entire second quarter of 2020, we have witnessed the commercial sales market dip down to its lowest activity since 2009. It has been a drastic U-turn, leveling off from the “Steady-as-she-goes” market we experienced between 2014 and 2019, to say the least.

From April through June we recorded just nine (9) total sales of commercial property on the South Coast, down from 15 during the same period in 2019, plus a substantial difference in dollar volume amounting to only $14.2 million versus $69.2 million for Q2 2019. It’s clear that in addition to fewer sales, we are seeing smaller price points on buildings. For example, the largest transaction of the quarter was the $3,696,000 sale of an industrial building at 5551 Ekwill St. in Goleta, purchased by an owner-user. And contrary to previous trends, six (6) out of the nine (9) sales were to investors. Most of these were development sites or were in escrow prior to the lockdown.

The pandemic and its effects on the economy in general has draped a blanket of inactivity over the market, keeping most investors on the sidelines and few owner-users poking their heads out for deals. Even in spite of low interest rates, lenders have been leery of granting new loans and may also be girding for possible defaults, making borrowing a tedious process at this time.

Another factor affecting our market is limited inventory. Retail continues to struggle as a result of the continued decline of brick-and mortar shopping. Now compounded by the pandemic, bankruptcies are showing up among even some of the biggest name retailers.

The best performing real estate sectors at the moment are industrial, apartments and a very hot residential market. Our data shows three (3) office sales, three (3) land, two (2) industrial and one (1) retail.

Going forward, much will depend on the outcome of the virus and the state of continued lockdown. When restrictions begin being lifted (and sustained), we expect to see a rise in activity due to pent up demand, as well as increased inventory in part due to some distressed properties coming to market as a result of vacancies and loss of rental income. As of now, there is an equal number of properties currently in escrow on our radar which may push numbers higher in the third quarter. Stay tuned.

Q2 2020 Leasing Summary

Office

Despite current events, Santa Barbara’s office market vacancy rate rose only slightly from 6.8% in Q2 to 7.1% in Q1. The average gross asking rate remained nearly unchanged at $3.13/SF, while the average gross achieved rate for new leases signed in Q2 dropped to $3.11/SF. The largest new office lease involved the 7,963 SF space at 4183 State St. which leased for $1.13/SF Mod GR. We also saw a drop in gross absorption from 41,000 SF in Q1 to 32,800 SF in Q2. No doubt the pandemic has cooled the market dramatically across all sectors, yet the minor increase in vacancy rate is a small relief for Santa Barbara office landlords.

Meanwhile in Goleta, not surprisingly vacancy increased marginally in Q2 to 6.1%, up from 5.4% in Q1. Still, for the sixth consecutive quarter Goleta’s office vacancy rate remained below Santa Barbara (7.1%). As in Santa Barbara, the slowdown in office leasing in Goleta was palpable with only three new leases completed in Q2, the largest at 125 Cremona Dr., Suite 100, with Aptitude Medical Systems taking about 8,100 SF. In fact leases at this address have been a bright spot during the pandemic as a handful of new deals have whittled down the previous 82,000 SF of vacant space to 32,000 SF between late Q2 and early Q3.

Moving down to Carpinteria, the office vacancy rate remained flat at 3.3% in Q2. Similar to the Goleta vacancy rate being below that of Santa Barbara, Carpinteria remains the low water mark on the South Coast, in part due to its small office inventory. No new leases took place during the second quarter and there are just four available offices spaces in Carpinteria, all of them located on Eugenia Place.

|

Industrial

The industrial leasing sector continues its story of stability on the South Coast, despite the Coronavirus threat that has stunted other sectors. In Goleta we did see the vacancy rate spike earlier this year primarily due to Skate One leaving 30 S. La Patera Ln. That said, the average lease rate has not seen much change on completed new leases.

There were only five (5) new industrial leases in Santa Barbara this quarter and two (2) in Carpinteria, due partly to the pandemic, as well as traditionally limited supply in both of those cities.

The largest industrial vacancy in the South Coast, the 102,000 SF mentioned above at 30 S. La Patera Ln., will mildly soften the industrial market in Goleta over the next couple of quarters until it is fully absorbed. We don’t see any other notable vacancies in the near term, so besides some of the available inventory in Goleta, the industrial sector should remain stable, both in terms of vacancy and continued stable lease rates. Industrial should be the least impacted sector throughout the time of COVID.

Santa Barbara Retail

During the second quarter of 2020 there were only four (4) new retail lease transactions totaling about 16,700 SF in Santa Barbara. Almost half of that square footage is attributed to Aqua-Flo’s 7,386 SF lease of the former Lumber Liquidator’s building at 18 S. Milpas St. Drawn by great identity, parking, a combination of high ceilings and open-layout indoor space, along with the ability to accommodate outdoor storage for building materials, this deal was emblematic of what appears to be somewhat of a surge in the trades industry locally.

Prior to the onset of the pandemic Santa Barbara’s retail vacancy rate was hovering around 3.5%. According to our Q2 analytics, the vacancy rate remains unchanged indicating that an equal amount of retail square footage came “off-market” for lease as came “on-market”. There is no doubt that bars, restaurants and other traditional retail establishments have been devastated by the onset of COVID-19 and the public fear, mandatory closings and limited occupancy that have come with it. As we await a vaccine and/or a meaningful drop in COVID cases, PPP loan funds dry up and assuming government mandated partial or full closures continue, expect to see a significant surge in retail vacancy between now and the end of the year.

On a positive note, the City’s decision to close State Street to vehicles and expand outdoor dining seems to have had a positive impact on retailers and given the public a reason to “take a stroll” downtown, increasing foot traffic on State Street and other parts of the downtown corridor. Continuing this practice and taking the next steps of making these blocks look less like “closed streets” with temporary vehicle barricades and more like inviting block-by-block paseos is an opportunity to consider as we seek to emerge from the pandemic and the retail challenges that were already facing downtown Santa Barbara pre-COVID.

West Ventura County Retail

We track just over 10 million square feet of retail property in West Ventura County. Vacancy rates have begun to steadily increase due to our current economic condition, currently at 4.51% in Ventura, 2.76% in Oxnard and 2.79% in Camarillo (Source: CoStar). Location is driving demand as tenants seek prime “main & main” locations. Retail boxes are a prime example as they continue to contract and reposition themselves in the market.

Ethan Allen will be relocating their Ventura location to The Collection in Oxnard, a more central position in the West Ventura County Market. Michael’s also relocated from a neighborhood center in Camarillo to a power center off the 101 Freeway, Camarillo Town Center.

Tenants most at risk that we are monitoring include Staples (Oxnard & Camarillo), TJ Maxx (Oxnard), Bed Bath & Beyond (Ventura) and 24 Hour Fitness (Ventura, Oxnard [2] & Camarillo).

Due to the pandemic, the grocery sector is red hot with dollars moving away from restaurants and into grocery stores. New grocers like Aldi, Grocery Outlet and the newest player in the grocery category, Amazon Grocer (Amazon’s new concept) continue to expand in our market. The new Amazon concept should be a major disruptor in the grocery category as they seek 35,000 – 40,000 square feet. As more competition enters the market, we expect there to be long-term fallout among more traditional grocers like Vons and Ralphs.

Ultimately As retail continues to move away from selling widgets to services, we see more medical (clinics, urgent care, chiropractic offices, optometrists) and dental moving into high exposure retail pad locations throughout the market and paying very competitive retail rents.

|

Q2 2020 Multifamily Investments Summary

The second quarter did not see a significant change in the volume of inventory coming to market. There has not been a rush by sellers to move properties as sellers seem to be more in a preservation mode at this time. That said, it has been a good time for sellers who have brought properties to market as the appetite for multifamily investment remains strong for well positioned properties.

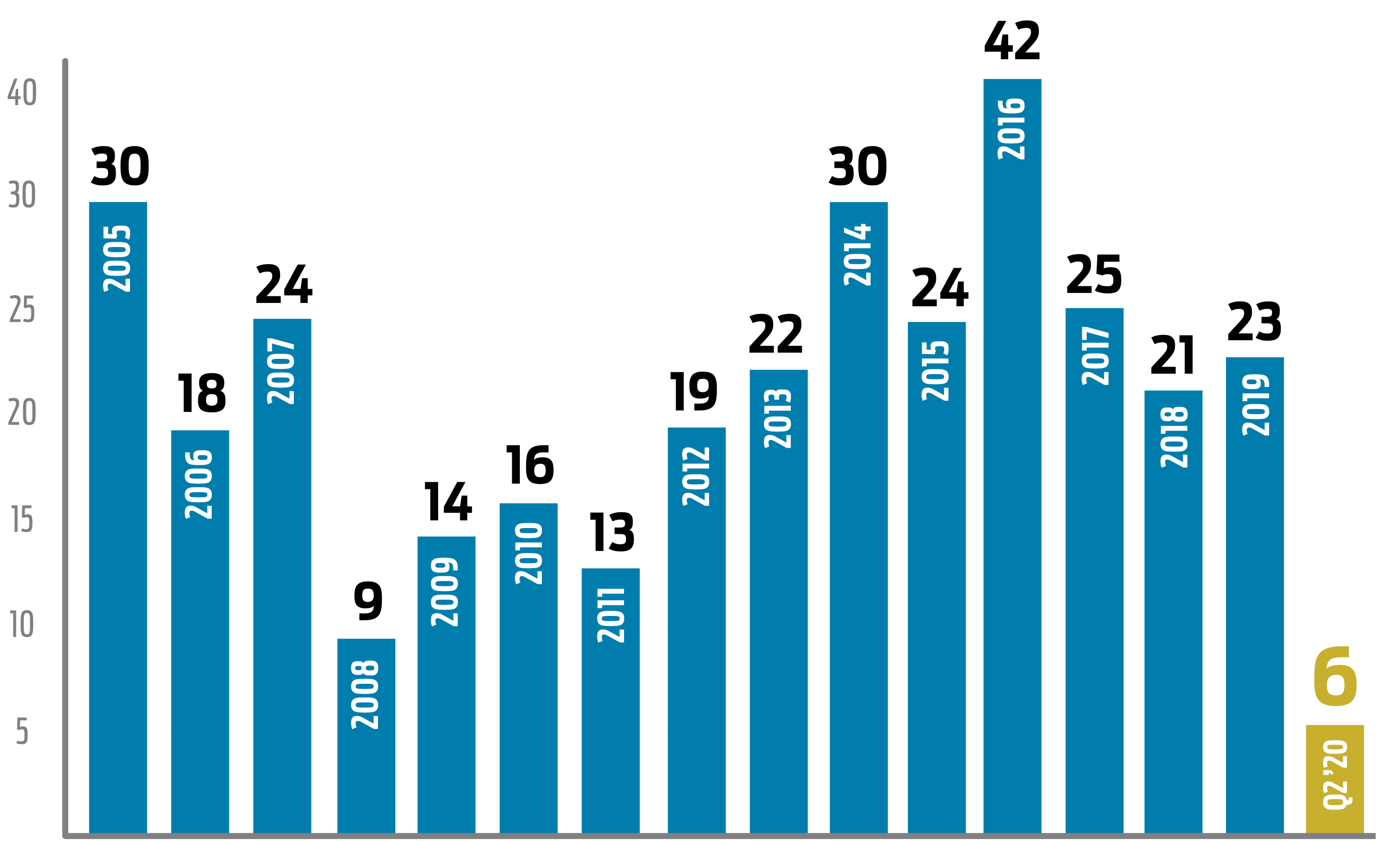

Still, sales activity is down overall in 2020 throughout the region. There were just eight (8) sales of properties 5-units or greater sold in Santa Barbara and Ventura Counties during the entire second quarter (including only three in South Santa Barbara County) versus the 13 that sold during the same quarter last year. Much of this can be attributed to fewer sales in Ventura County and Northern Santa Barbara County as there hasn’t been the same inventory in those markets. In fact over the first two quarters of 2020 we recorded just six (6) sales total of 5+ units in size in South Santa Barbara County compared to 10 during the same period last year, representing a 40 percent decrease. Part of this trend of fewer sales could be due to the larger impact of COVID-19 which industry analysts are still trying to get a handle on.

As of the end of the second quarter, there were only six (6) properties of 5+ units in size available along the South Coast and two were in escrow.

In Ventura County there were three (3) sales of note during Q2, two mid-size buildings between 20–30 units and another very large asset of 272 units sold in Oxnard. One of the two mid-size deals that closed was 300 N. G St., a 20-unit asset that sold offmarket in Oxnard. The buyer was in a 1031 exchange and the sale price represented an approximate 5% cap rate. The other deal was a 33-unit complex, also off-market, and that sold for $8,075,000 and a 5.18% cap rate. The property was purchased by a local Ventura investor. The 272-unit property that sold in Oxnard at 2000 E. Gonzales Rd. was a luxury apartment complex owned under the “Artisan” brand that sold to an institutional investor. That deal sold at $339,000 per unit, very much on the upper end of the spectrum for Oxnard, and continuing the upward trajectory of investment in the area.

While not much inventory transacted in Santa Barbara County during the quarter, there are signs of life in the market and it is still apparent that multifamily, especially South County Santa Barbara multifamily, is very much in demand. An example of this was an exchange investor purchasing a 10-unit property in Santa Barbara’s coveted West Beach neighborhood at 204 W. Yanonali St., at $5,650,000 and a 3.5% cap rate, nearly $1M more than it was purchased for in 2019. These well-maintained complexes in Santa Barbara continue to be prime targets for exchange investors seeking stability, and they are willing to pay high valuations to get their hand on these assets.

While the credit markets were temporarily stemmed during the initial onset of the pandemic, interest rates are now at near 50 year lows, and lenders are able to get more aggressive on underwriting. This is allowing more deals to pencil and as we speak, more deals are picking up traction. Expect Q3 to see more transaction activity and.

Recent News

Pacific Coast Business Times: CRE: American Riviera Bank buys Ventura branch office

Most banks lease their local branches and standard offices, but American Riviera Bank decided to go against the grain, announcing that …

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …