Please download the complete Q3 2020 market report here or contact your Radius broker for more information.

|

Q3 2020 Commercial Sales Summary: All aboard the roller coaster

This year has been anything but predictable, so we’re throwing all forecasts out the window and reporting facts, just the facts.

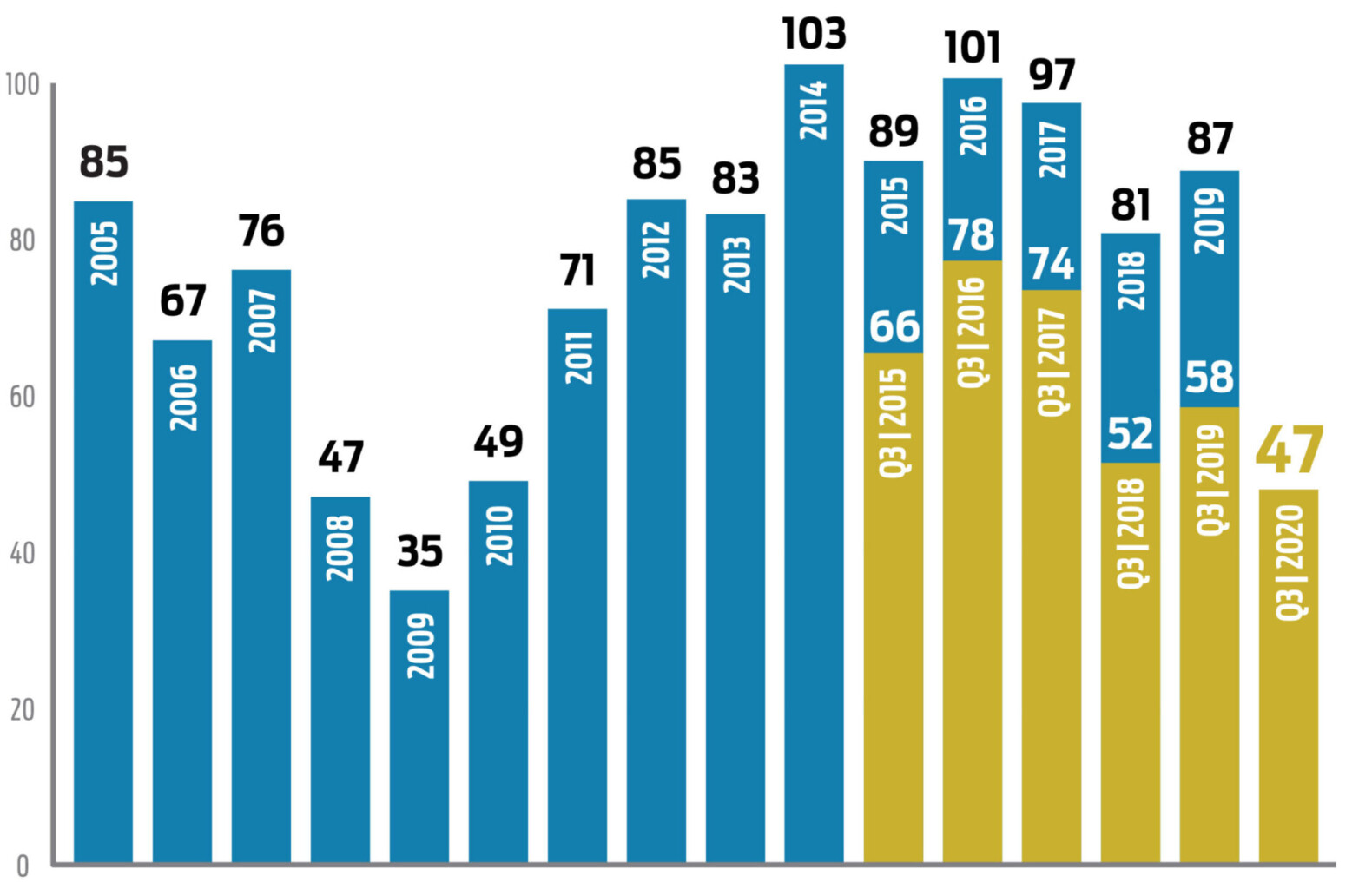

The third quarter 2020 commercial sales numbers were refreshingly positive compared to the beginning of the year. When compared to Q3 2019, the activity was surprisingly similar: 23 closings resulting in $115MM in volume in 2020 vs. 27 transactions totaling $146MM in 2019. Considering all that the country and economy have been through over the past several months, this is truly remarkable. In fact, you may also be surprised that Q3 sales are very close to average quarterly sales for all but recession years.

We might liken 2020 to a roller coaster none of us ever want to ride again. The year started with a reasonable 15 sales in Q1, before quickly plummeting to just nine (9) sales in Q2, only to ratchet steadily back up to the third quarter’s peak of 23. Dollar volume followed this same path: $39MM in Q1, down to $14MM in Q2, then rocketing back up to $115MM in Q3.

That said, 2020 year-to-date numbers compare less favorably to the same period in 2019: 47 total sales for 2020 at $169MM volume vs. 58 sales and $320MM in 2019. Clearly and not unexpectedly, Covid has taken its toll this year.

Of the 47 sales to date, 22 were office, seven (7) were industrial, 11 were retail, five (5) land and two (2) hotels. We feel these numbers show a certain resiliency in the individual categories, even for retail which has been beaten down recently.

So what does all this tell us about the market? It seems that once the Covid scare was “understood” and measures were taken to mitigate the damage, the market started to recover the momentum that was in place at the end of 2019 and the first couple of months of 2020. Certainly the government stimulus plans helped, including historically low interest rates, but also a continuing measure of confidence in our South Coast commercial market in particular.

Once again this confidence is supported in large part by the number of owner-user sales that continue to drive sales. This quarter alone over half of the sales were to owner-users and for the year almost two-thirds of the sales were to this group, supporting the trend of investors taking a more conservative approach because of uncertainty in proforma income streams and users taking advantage of properties with vacancies.

The other interesting phenomenon that has been with us for a while is the number of off-market transactions. While the statistics are not always available, it seems that roughly one-third of the sales have been for properties not actively marketed at the time of sale.

Finally, we can’t conclude this narrative without commenting on State Street retail. Sales for the formerly prime, downtown retail corridor have been non-existent, partially due to lack of inventory, but also due to skepticism from investors. That said, there still were nine (9) State Street sales for the year, six (6) of them in Q3. Most, however, were outside the central core between the freeway and Micheltorena Street.

Q3 2020 Leasing Summary

Office

During the third quarter, Santa Barbara registered its highest office vacancy rate since 2003 at 7.7%, up from 7.1% in Q2. During the start of the fourth quarter a few additional spaces have also come to market. At this point there has not been a noteable change in lease rates, hovering at $3.12/SF average gross asking.

The future of the office sector remains uncertain as many tenants are simply in a wait-and-see mode as to how they may modify their businesses in response to Covid-19.

The largest lease of the quarter was NS Ceramics taking 7,259 SF at 602 E. Montecito St., with a total of approx. 42,751 SF absorbed during the quarter on 26 leases.

Moving up to Goleta, during the third quarter the office vacancy rate jumped to 7.8% from 6.1% in Q2, largely due to LogMeIn selling and vacating their former campus on Hollister Ave. At the same time they were vacating, the largest lease of the quarter took place at 7410 Hollister Ave. with a local tenant taking approx. 21,793 SF. Two other deals of note were Apeel Sciences taking 13,193 SF at 120 Cremona Dr. for one year, and Skate One doubling their size at 6860 Cortona Dr. Overall the market was active with 27 new leases signed in the 3rd quarter. But while Goleta is traditionally known for leasing larger floorplates, 13 of those 27 leases involved spaces under 3,000 SF.

Finally, in Carpinteria the office vacancy rate climbed to 6.1% by the end of the third quarter, up from 3.3% in Q2. There was only one new lease signed, a 2,396 SF space at 1110 Eugenia Pl. While ProCore did put approximately 50,000 SF on the market for sublease, their buildings were more industrial. The largest available true office space is a sublease of 8,896 SF on Cindy Lane. In 2021 we may likely see the amount of available space will continue to include a fair number of sublease opportunities as tenants adjust their needs for in-office personnel.

|

Industrial

Santa Barbara’s industrial vacancy rate has remained low and steady over the last several years, always within a percentage point. We did see a slight uptick from 1.0% in Q2 to 1.4% in Q3, which is technically the highest vacancy rate we have seen in a number of years for this low-inventory market. The average gross lease rate on new leases dropped from $2.45/SF in the second quarter to the current $2.06/SF.

There were a total of seven (7) new leases totaling 16,492 SF during the second quarter including the largest at 820 Bond Ave., a sublease of 7,528 SF. Again, there remains slim pickings for prospective tenants with very low inventory; in fact there are currently only 10 vacancies totaling just over 68,399 SF. We do expect inventory to remain tight, but depending on demand and the design/function/condition for each vacancy, lease rates may continue to fluctuate.

Meanwhile in Goleta, the industrial vacancy rate has continued a downward trajectory since the beginning of the year, falling from 9.3% in Q1 to 6.8% in Q3. The drop in the last quarter was primarily due to 75,453 SF total being absorbed in the market. In fact there were two noteworthy larger leases signed in the second quarter, including 25,623SF leased by Lockheed Martin at 340 Storke Rd. and 25,940 SF leased to Hazelwood Storage at 6338 Lindmar Dr. It should also be noted there will be approx. 96,323 SF of flex space coming online next quarter with the end of the LogMeIn lease at 7418 Hollister Ave. The average gross asking rate remained stable at $1.58/SF and should stay stable even with the expected increase in vacancy.

Moving down to Carpinteria, the industrial sector saw a 5.0% jump in vacancy over the last quarter from 2.8% in Q2 to 7.8% in Q3, which can happen in this low inventory market. There were just two leases executed in the third quarter for a total of 5,762 SF, compared to the six current availabilities totaling 34,286 SF. It should also be noted there is currently 67,330 SF of sublease space available with Procore representing approx. 52,830 SF of it.

In tandem with the increase in vacancy, there has also been contrast as seen in the increase in the industrial vacancy there has been an increase in the average gross lease rate. Just as the vacancy rate increased, we also saw a rise in the average gross achieved rate moving from $1.05/SF in Q2 to $1.44/SF in Q3. Due to continued demand for industrial space throughout the greater South Coast market we believe that lease rates will remain competitive and stable in the Carpinteria sub-sector.

Santa Barbara Retail

There continues to be little to celebrate on the retail front as Santa Barbara’s retail sector remained stagnant during the third quarter with just five (5) new leases signed, including one on Coast Village Rd. in Montecito. The most significant Q3 lease was at 110 Anacapa St., Santa Barbara for 1,350 SF where clothing boutique Dylan Star opened their Funk Zone location. Lease space for the quarter totaled a mere 5,351 SF, making very little impact on the market with nearly 400,000 SF of vacant retail space currently remaining on the market.

That said, from a year-over-year perspective, the 3.7% Q3 2020 retail vacancy rate actually decreased slightly from 3.9% in Q3 2019. The average gross asking rate during the third quarter was $4.17/SF, with the actual achieved gross rates averaging $3.56/SF.

Activity in the downtown State Street corridor remains tepid at best, despite the new “State Street Promenade” that has taken shape to allow merchants and restaurants more opportunities to adapt to the new Covid era. The vacancy rate in that sector crept up to 16.87% in Q3 from 13.25% in Q2 (see Page 6 for details). Still, one bright spot for the area is a recent long term ground lease at the site of the former Staples at 410 State St. While the retail portion of the property will remain, the city has granted tentative approval of 84 apartment units to be constructed on the parking lot between the Staples building and the Reid’s Appliance building, some much needed good news as we seek to inject new life into the ailing downtown corridor.

|

Q3 2020 Multifamily Investments Summary

Santa Barbara South County

The third quarter saw some sense of normalcy return to the local multi-family investment market. Investors mostly snapped up assets in the 2- to 4-unit range, with a few sales above 5+ units. As usual, not much inventory came to market, though the assets that did tended to have multiple offers and generally sold quickly. For example, 410 E. Islay St., an upper Eastside duplex sold for $1,295,000, and 1615 Garden St., a duplex in a similar location sold for $1,040,000; both garnered a lot of activity upon coming to market. Similarly, a 3-unit property at 615 W. Mission St. entered the market near the end of the quarter, also with multiple offers. Another 3-unit asset at 1418 Almond St. also closed, the result of an off-market deal. Lack of inventory, low interest rates and increased migration to Santa Barbara has spurred a hot single-family market, further impacting this flurry of activity for assets in the 2- to 4-unit range.

As mentioned, on the larger side (properties 5+ units), there were just three (3) deals on the South Coast and the general lack of inventory again made for a less than normal amount of transaction volume for the quarter. In Summerland, an 8-unit asset located at 2380 Lillie Ave., was the largest sale at $2.3 million. In Santa Barbara a 5-unit property at 213 Ladera St. sold for $1,495,000 with an in-place cap rate of approx. 3.5%. That general neighborhood on Ladera has seen increased investment activity over recent years as many buildings on the block have been rebranded to focus on student housing. For example, 305 Ladera St., a 3-unit town-house style property, which is also a student housing asset with possible development potential.

Despite the smaller number of larger properties that traded on the South Coast, there are some hints that we will see movement in this area. A 22-unit asset located at 6681 Berkshire Terrace, Isla Vista went to market at $7,495,000 with multiple offers and is currently in escrow. There are also some indications of a few other larger assets coming to market in the downtown area that will likely garner much interest. Moving forward we do expect the market to pick up speed, with most assets in our area seeing a good deal of activity.

Santa Barbara North County

In the North County, a few larger assets sold during Q3, including 212 N. O St., Lompoc, an 8-unit asset which traded for $1,292,000 or $161,500/unit at a 5.11% capitalization rate. The North County has been a bit more impacted by Covid-19 with minimal activity, although investors are still on the lookout for slightly higher yielding assets in this region.

W. Ventura County

In western Ventura County, four larger assets sold during the quarter, the largest by far at 5505 Cochran St., Simi Valley. This 254-unit complex traded for almost $36 million and was part of a larger asset sale of properties across the country.

A 10-unit asset at 113 W. Ramona St., Ventura had come to market in previous quarters, and finally traded at $2.0 million or $200,000/unit at a 6.08%. cap rate. Another notable sale was 901 Peninsula St., Ventura, a 12-unit asset which traded for $3.9 million, resulting in a slightly above average price-per-unit for Ventura at $325,000/unit. Like Santa Barbara, Ventura is still very much in demand, and although sales in the 10+ unit range are more frequent, 20+ unit assets remain extremely hard to find.

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …