|

Q4 2021 Commercial Sales Summary: So. Coast Sales Buck Pandemic

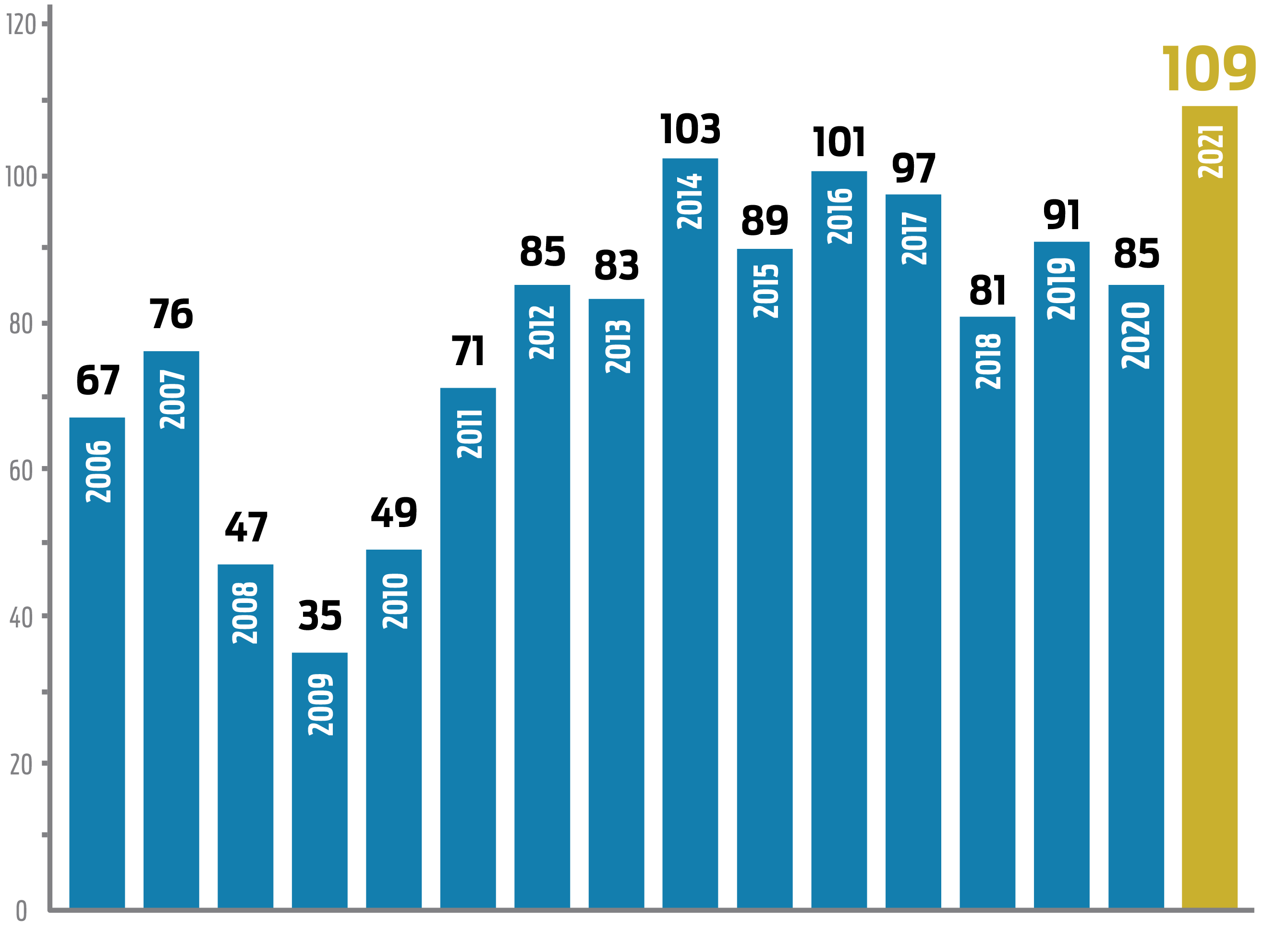

Surge in Q4 deals helps boost 2021 with record 109 sales & $556MM volume

Market trends and momentum persisted on the South Coast throughout the fourth quarter, closing 2021 on a high note and capping a year that produced both a record number of commercial sale transactions and dollar volume.

While Q4 is typically the most active quarter any year, the last three months of 2021 were especially prolific given the current economic climate. Not surprising, there was strong motivation by many to close on deals before year-end, in part fueled by uncertainty of what direction 1031 Exchange and Capital Gains laws were potentially headed in 2022.

The final quarter of 2021 saw a robust 43 total sales with $335MM in volume, compared to Q4 2020 (29 sales at $198MM) and 2019 (32 sales at $217MM). The category breakdown for Q4 split relatively evenly at 11 retail, 11 office and eight (8) industrial sales, followed by six (6) land, four (4) specialty/hospitality, two (2) hotel and one (1) healthcare/convalescent sale.

For 2021 in total, there were 109 commercial sales —well above the 15-yr. average of 77.3 sales per year—with dollar volume at $556MM, punctuating the strongest year to date on record for the South Coast. This represented a 43% annual increase in dollar volume over 2020 which closed with 85 sales at $386.5MM. The previous record was achieved in 2014 which registered 103 sales and $439MM.

In addition to a consistent lack of inventory, there were a handful of other notable trends that persisted throughout 2021. For one, investor buyers dominated the market in comparison to owner-user buyers (30 / 13 respectively), while 37% of all transactions were off-market (16 total). We should emphasize that, contrary to popular belief, most of these off-market properties sold at a premium.

Another noteworthy trend is the increase in number of retail properties sold, with 11 in Q4 alone. Given the state of the retail sector in general, which was exacerbated by the pandemic, it’s not surprising that we’re seeing increased interest from investors wanting to reposition retail property to other best uses. Case in point being the sale of the Nordstrom building at Paseo Nuevo Mall in downtown Santa Barbara which traded to a group of out-of-market investors. At a $13MM price tag it was relatively small on paper compared to other giant deals during the year, yet it may have an outsized impact on the leasing market moving forward. While new ownership remains hush on their plans, it’s very possible we’ll see a very large chunk of the 3-story building converted to office use—similar to the former Macy’s property in the same mall—driving up an already hefty office vacancy rate. More on that in the office leasing summary of this report.

Finally, 2021 saw the local hotel industry bounce back resiliently from COVID. Drive-to tourist markets outside of major cities, such as Santa Barbara, are benefiting from travelers wanting to stay local rather than risk COVID complications by going abroad. As a result, local hotel occupancy rates have returned to near pre-pandemic levels and we are seeing average daily rates (ADR’s) for some hotels beat 2019 highs by nearly 20%. Hotels are a great hedge against inflation. As such, there is increased interest from buyers for local hotel assets. During the fourth quarter alone we saw two (2) hotel sales (Hotel Santa Barbara and Hotel Indigo) in a town where typically we see one or two trade in a year. Both hotels received multiple offers and traded at arguably stronger valuations than they would have in 2019. Additionally, there is a 50-bed hotel in West Beach that received multiple offers and is currently in escrow.

Looking forward, the supply and demand fundamentals for quality assets continue to be out of balance, a trend we are seeing nationally, and this looks to continue into 2022. The key element to watch this year will be interest rates, which are expected to rise and will likely affect CAP rates and prices. However, if the current buyer demand persists, the forecast looks to be another strong year on the South Coast.

Notable Q4 Sales

- 3805 State St., Santa Barbara ∙ ±230,689 SF Retail at La Cumbre Plaza Mall ($64MM) Off-market

- 527 State St., Santa Barbara ∙ 75-key Hotel Santa Barbara ($41.9MM)

- 71 S. Los Carneros Rd., Goleta ∙ ±105,257 SF Ind./R&D Leased to Apeel Sciences ($36.2MM) Off-market

- 121 State St., Santa Barbara ∙ 41-key Hotel Indigo ($18.75MM)

- 817 State St., Santa Barbara ∙ Former Nordstrom Building in Paseo Nuevo Mall ($13.09MM)

- 111 E. Victoria St., Santa Barbara ∙ 19,597 SF “Class A” Downtown Office Building ($12.25MM)

- 21 E Victoria St., Santa Barbara ∙ 13,784 SF Downtown Office Building ($10.3MM) Off-market

Q3 2021 Leasing Summary

Office

After the high watermark office vacancy rate of 10.8% for Santa Barbara in Q2 2021, this figure edged down over the last two quarters landing at 9.2% to close the year. As noted in previous reports, roughly 87,500 SF of this vacant space sits in the former Macy’s building which anchors the Paseo Nuevo Mall and is currently marketed as office use rather than retail. Without this space the vacancy rate would be a more traditional 7.5%.

While we’re on the odd subject of discussing big box retailers in the office market summary, one new wildcard is portions of the 3-story Nordstrom space in the same mall. We hear the upper levels may come to market for lease as creative office space, though ownership is tight-lipped on plans which could include other uses. If this happens it could mean roughly 100,000 SF of office space hitting the market which will increase vacancy substantially. A hit or miss? Time will tell, but it’s encouraging to see investors doing their part to think outside the (big) box to breathe life into the downtown corridor.

|

While not new leases, the largest office transactions during the fourth quarter included Ontraport extending their lease of 23,000 SF in the Riviera Business Park, followed by Well Health also extending their lease of nearly 15,000 SF at 1025 Chapala St. Though neither deal resulted in absorption, it’s nevertheless a win when businesses stay in the market and square footage stays out of the vacancy column.

Down to Capinteria, the office vacancy rate currently stands at 3.9%, up slightly from 1.9% at the end of the third quarter. You’d never know vacancy is that tight driving around Carpinteria with parking lots at ProCore and LinkedIn nearly vacant as both continue to operate remotely. The only new lease in Q4 was 1,450 SF at 4195 Carpinteria Ave., while the largest available space is 8,900 SF at 6398 Cindy Ln. Noteworthy is the Q4 sale of the entitled Lagunitas property at 6380 Via Real. Hopefully that 80,000 SF building will be built in the next 18 months.

Moving on to Goleta, the office market continues to tick along with a vacancy rate of 6.6% at year end, lower than the year started. Goleta saw just four (4) new leases in Q4, the largest being the 6,471 SF lease at 150 Castilian Dr., Suite 100 to Serimmune, Inc. There are currently 30 spaces for lease and the vast majority of the vacancies are under 10,000 SF. The largest vacancy on the market is the 38,183 SF at 326 Bollay Dr. We can expect to see the office vacancy rate continue to lower as spaces lease and employees return to work.

Industrial

The South Coast industrial sector continues to remain stable with very low vacancy and steady lease rates. The majority of Q4 leasing activity took place in Goleta with five (5) new leases totaling almost 42,000 SF, including three (3) leases just over 10,000 SF each at 30 S. La Patera Ln., backfilling the space vacated by Skate One. All three leases represented expansions by companies including OSI Hardware. There remains 31,000 SF vacant at this property. The largest Goleta vacancy was 7418 Hollister with 49,000 SF. Vacancy in Goleta dropped to 2.7%in Q4, continuing a strong downward trend from just over 9% in early 2021.

Santa Barbara had two new leases with the largest being Kopu Water at 4179 State St. for 8,617 SF. The quarter ended with five (5) industrial vacancies in the city but that still equates to only a .6% vacancy rate for the market. After years of increasing rates we seem to have stabilized to flat rates in this sector.

Carpinteria, our smallest submarket, did not see any new industrial leases and sits at just four (4) vacancies, the largest at 6384 Via Real with 24,000 SF, but we expect that to lease soon. Carpinteria’s industrial vacancy represents 3.7% which was up just slightly for the quarter.

Industrial leasing will continue with stable rates and very limited supply. With ongoing industrial demand, we are hopeful to see new development applications, however there is limited undeveloped industrial land.

Santa Barbara Retail

During the fourth quarter, there were seven (7) new retail leases signed totaling about 58,000 SF (two less than were signed in Q3 but 31,000 SF more of retail absorption). These lease transactions ranged in size from approx. 700–45,000 SF. The most notable was a 45,000 SF lease to Aloha Fun Center at 710 State St. (former Macy’s building). It has been reported the tenant will feature roller skating, laser tag and an arcade. Another notable lease occurred at 401 W. Carrillo St. (former Big Brand Tires). That approx. 4,341 SF building was leased to a tenant that will be announced publicly shortly.

On the vacancy front, Santa Barbara’s retail vacancy rate dipped from last quarter’s 4.3% to 3.5% (driven mainly by the lease of the former Macy’s building). With this drop in vacancy rate, not surprisingly asking rates have ticked upward from Q3’s $4.14/SF Gross Equivalent to this quarter’s $4.21/SF Gross Equivalent (Base Rent + NNN). Achieved Rates declined fairly substantially going from Q3’s $5.75/SF Gross Equivalent to $3.71/SF in Q4. With limited lease transactions occurring, achieved rates can fluctuate dramatically. The current $3.71/SF is in line with the $3–$4 Gross Equivalent achieved rates we have been tracking since Q4 2020. The true market rate of a retail building/space is dictated by the specific location and size of the retail asset (contact your Radius representative regarding your retail property).

By the end of Q4 there was approx. 372,000 SF of retail space for lease in Santa Barbara (down from Q3’s 449,000 SF). With leasing of 45,000 SF of the old Macy’s space and the recent Q1 2022 leasing of approx. 70,000 SF of the old Sears property in La Cumbre Plaza, expect retail vacancy possibly to continue downward locally as we move through 2022.

One thing to keep an eye on is how the new owner of the approx. 175,000 SF Nordstrom property in downtown Santa Barbara will choose to market that property. It has been reported that the owner, who acquired the long-term ground lease of the property in Q4 2021, “believes there is a better use of this space than big-box retail, which has been highly impacted by e-commerce.” They have stated that their plan “might include a smaller amount of retail, or no retail, and other uses including creative office” and that their goal is to “breathe new life into the building and the surrounding neighborhood.” How this space ends up being marketed will dramatically impact the supply of vacant space and the vacancy rate of either Santa Barbara retail or downtown Santa Barbara office during 2022, as mentioned above.

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …