Please download the complete Q3 2019 market report here or contact your Radius broker for more information.

|

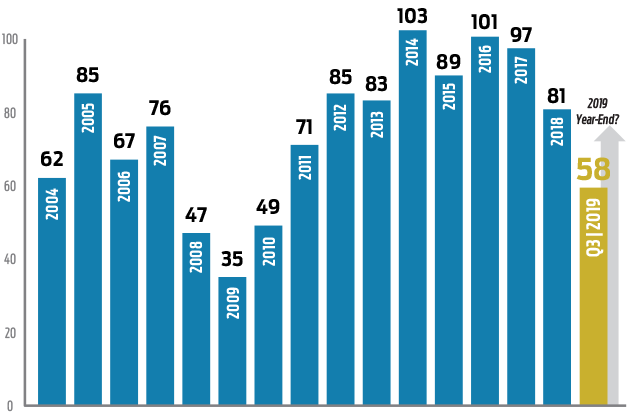

Q3 Commercial Sales Summary: The Goldilocks Effect, Again

It seems that 2019 commercial sales numbers are following the same script as 2018 in almost every aspect except for dollar volume.

Total sales for the first three quarters of 2019 were 58, just one more than the same period in 2018. Even the number of sales in each commercial use category (office, retail, industrial, land) are similar, with the only somewhat notable statistic being the decline in land sales. This may be attributed to dramatic increases in construction costs, but also to the dearth of land sales in general in our development-challenged South Coast environment.

The big difference between 2019 and 2018, however, is the dollar volume to date. For Q1-Q3 2018 this figure was $184,833,720 with an average price per transaction of $3,243,000. But in 2019 this figure has soared to $320,445,000 total with an average price per transaction of $5,525,000.

Simply averaging the price per deal is, of course, a little misleading. Still, the trend seems to be a steady number of sales each year with prices increasing somewhat, accompanied by a disproportionate number of larger properties selling, leading us to believe that the market is still going strong and steady without flying off the handle.

When we dig deeper into the stats, however, we begin to see that the more interesting story is the number of sales to buyers intending to occupy the property (owner-users) is virtually equal to the number of sales to pure investors. This has essentially been true for both 2018 and 2019.

Since most owner-user sales have relied on leveraged financing, low interest rates have certainly contributed to this activity. Some of the investor purchases today may be viewed as hedges against a dramatic decline in the stock market. How else do you explain multiple offers and well-located assets that are priced in the mid-4% Cap Rate range?

Overall the sentiment among investors seems to be that while the recession cloud seems to be ever-looming (at least according to the media), the outlook still seems positive for well-located, secure investments on the South Coast.

We think this fear of recession combined with a lack of inventory is what is creating a tale of two markets. Less risky leased investments with quality tenants are trading at premiums and vacant buildings with perceived risk are trading at discounts.

Some prime examples include 3793 State St. This property was leased to Fidelity and traded for $4,250,000 at a 4.8% Cap that translates to $949/SF, a big number for upper State Street. Similarly, 6300 Hollister Ave. in Goleta was a 100% leased office/R&D building that sold for $33,165,000, which was $312/SF and a 6.5%, Cap Rate. Finally, 6410–6460 Via Real in Carpinteria was purchase by the tenant, Microsoft, for $30,411,162, which was $349/SF. These are all historically huge prices per square foot pushed by low Cap Rates.

Alternative examples include downtown retail properties, which some perceive to be more risky investments. For example, the sale of 1013 State St. which was vacant and sold for $1,290,000 at $427/SF. Additionally 125 E. Victoria was a well-located vacant office building that sat on the market for 14 months, went through several price reductions and ultimately sold for $3,800,000 or $443/SF.

In the current market if a building has a meaningful amount of existing vacancy (or pending vacancy) and has deferred maintenance which will need to be addressed now or in the near future, unless those assets are priced very competitively they are sitting on the market for longer periods than in the past (often with multiple price reductions) as investors and owner-users are showing less of a propensity to “stretch” on valuation as they might have in the past.

|

Notable Q3 Sales

6300 Hollister Ave., Goleta (Office)

Largest sale of 2019 to date. | 106,309 SF | $33,165,000 | $312/SF | 6.5% Cap

6410-6460 Via Real, Carpinteria (Office)

87,138 SF | $30,411,162 | $349/SF | 5.44% Cap

827 State St., Santa Barbara (Retail/Office)

58,762 SF | $23,575,000 | $401/SF | 4.93% Cap

1486 E. Valley Rd., Montecito (Retail)

6,357 SF | $13,000,000 | $2,045/SF | 7.43% Cap

2323 Oak Park Ln., Santa Barbara (Office)

7,625 SF | $6,250,000 | $820/SF | 5.0% Cap

3793 State St., Santa Barbara (Retail)

4,477 SF | $4,250,000 | $949/SF | 4.8% Cap

|

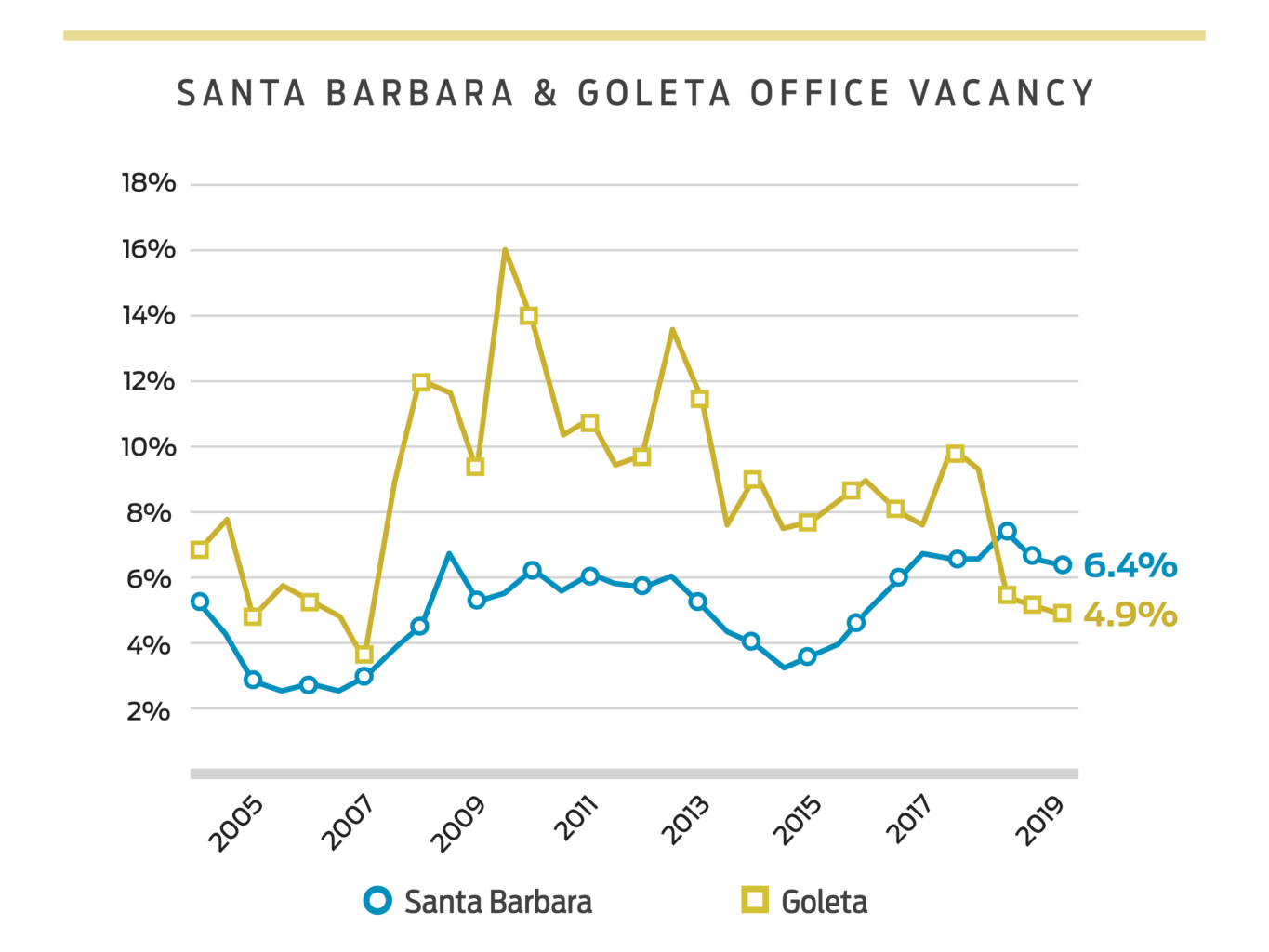

Q3 Leasing Summary: Santa Barbara Office vacancy rate at 6.4%, still trending higher than Goleta since 2018

Office

Not much has changed in Santa Barbara’s office leasing market over the past few years, with the vacancy rate fluctuating between 5.6 percent and 7.4 percent from the third quarter of 2017 to date. In fact office vacancy dropped just slightly since the second quarter of 2019, going from 6.6 percent to its current 6.4 percent.

The largest office property on the market at this time is 402 E. Gutierrez St., available for sublease at approximately 26,339 square feet. Notably, of the roughly 120 spaces available for lease at the end of the third quarter (approx. 330,000 square feet total), only 13 are larger than 5,000 square feet, with the vast majority of spaces continuing to be smaller than 3,000 square feet. Indeed property owners with spaces in this size range in need of TLC may continue to see those spaces sit vacant.

While the average gross asking rate had a minor decrease from $3.16/SF in Q2 2019 to $3.11/SF in Q3, the average gross achieved rate rose substantially from $3.18/SF to $3.35/SF.

The largest new office lease of the quarter involved 111 W. Micheltorena St., suite 300, an approx. 6,147 SF space leased by Bragg Live Food Products, the world’s top apple cider vinegar producer based in Santa Barbara and now partially owned by celebrity couple Katy Perry and Orlando Bloom. Yet perhaps the most notable development in the office sector involved a space leased last year. The converted retail property at 1001 State St. is now officially occupied by Amazon, continuing the trend of tech companies moving into the downtown area.

Moving on to Goleta, the office vacancy rate also declined slightly from 5.2 percent in the second quarter to 4.9 percent at the end of Q3.

Unlike Santa Barbara, this market continues to be driven by larger vacancies, with the largest of all being the 82,132-square-foot space at 125 Cremona Dr., which accounts for roughly 40 percent of the market’s vacancy (210,000 square feet). The average gross asking rate also ticked down a little, from $2.10/SF to $2.08/SF from the second to third quarter. The average gross achieved rate saw a skip from $2.05 to $2.09/SF.

The most notable new leases of the quarter involved Intouch Health taking 28,025 square feet and 17,177 square feet at 7402 Hollister Ave. and 7410 Hollister Ave. respectively. While Goleta has a diverse mix of vacancies in different size ranges, we may expect to see quality spaces in the 2,500–3,000 square foot range dominate the leasing over the next quarter.

Down south to the Carpinteria market, the office vacancy rate increased dramatically in the third quarter from 1.5 percent to 3.9 percent. In such a small inventory market, it only takes a few vacancies to move the needle significantly and they all seem to be on Eugenia Place at the moment. Still, the largest vacancy is only 7,407 square feet at 1145 Eugenia Pl.

The average gross asking rate raised from $1.64/SF to $2.19/SF and surprisingly there were no new leases in Carpinteria last quarter. We do expect a few more vacancies to be filled this quarter, likely bringing the vacancy rate back near the 1.5 percent mark.

|

Industrial

The City of Santa Barbara’s industrial vacancy rate has moved very little over the past few years, now sitting at just 1.1 percent. Indeed the market continues to be defined by a lack of industrial inventory.

As such, gross lease rates tend to vary with only a handful of transactions occurring each year. Rates will vary depending on size, parking and condition of each property.

Only two new leases were executed during the third quarter totaling 2,900 square feet, with an average gross rental rate of $2.68/SF. Currently there are 11 spaces on the market in Santa Barbara accounting for approximately 52,800 square feet and ranging in size from 1,204 square feet to 14,368 square feet.

Notably, Santa Barbara is a unique market that over the past several years has seen an influx of interest in different uses that began with the Funk Zone and quickly moved its way to the up-and-coming self proclaimed Lagoon District, the commercial and residential neighborhood centered around the Haley Street corridor and bound by Garden, Cota, Milpas, Montecito and Anacapa Streets. Commercial landlords have taken note of this demand for space and it appears a rent threshold has been reached. Traditional industrial uses are not able in many cases to justify current rental rates that are now often equal to office and retail rates in the market. So with industrial space in some areas even more scarce than it was before, landlords will need to remain realistic about what industrial users can agree to and sustain long term.

Moving north to Goleta, the industrial vacancy rate rose slightly from the previous quarter from 5.4 percent to 6.2 percent at the end of Q3. While this is actually more than double where we were two years ago when the vacancy rate was at 2.6 percent, vacancy is still in a healthy range and as a result rates have remained steady with the average gross achieved rate for Q3 at $1.58/SF and the average gross asking rate for available properties at about $1.63/SF.

There were just seven new leases signed during the third quarter comprising about 38,800 square feet, with the largest and most notable being Deployable Space Systems taking approximately 12,600 square feet at 165 Castilian Dr. There remains roughly 260,500 square feet of space on the market from just 18 listings.

We believe industrial lease rates in Goleta will remain level throughout the rest of the year. The greatest demand for space remains in the sub-15,000-square-feet range.

Meanwhile down in Carpinteria, the industrial market has seen very little movement since the start of the year, in fact there were no new leases signed during the third quarter. There are also currently only three spaces available in Carpinteria ranging from just 700 square feet to 1,450 square feet. Slim pickings, and this is the norm for the market. But there is some discussion that a potential mid-size industrial tenant may be exiting the market which may play out sometime in the next two quarters and would likely cause a spike in vacancy at the time given the sheer lack of inventory in the market.

Retail

This time last year we reported that we expected to see an increase in leasing activity with landlords getting more aggressive to secure tenants in the sluggish retail market. In fact there was a significant increase in retail leasing activity during the third quarter of 2019 versus Q3 2018, with 14 new leases signed comprising a total of 30,600 square feet. In third quarter 2018 we recorded just seven new leases totaling 9,687 square feet.

The average gross achieved rate during the third quarter was $4.24/SF compared to $3.99/SF a year ago. That said, this figure was propped up by four leases in Montecito which averaged $5.89/SF gross, so if you factor out Montecito then the average achieved rate for Santa Barbara drops down to $3.58/SF gross.

Moving on to inventory, at the end of the third quarter there were 86 properties on the market for lease totaling 405,664 square feet, with an average gross asking rate of $4.16/SF. This is similar to Q3 2018 when there were 89 properties available, yet lower total square footage at 380,431 square feet.

For the Santa Barbara retail market, which includes Summerland and Montecito, the vacancy rate has remained stable over the past year, increasing slightly during the third quarter, from 3.6 percent a year ago to the current vacancy rate of 3.9 percent.

Two final notes. First, there has been an increase in temporary or Pop-Up tenants on downtown State Street, which suggests more willingness on the part of landlords to sign short term leases. Secondly, due to the ongoing challenges that retail tenants in this market face when trying to obtain building permits for improvements, the City of Santa Barbara has hired a business liaison to help facilitate the permitting process. While it remains to be seen just exactly what steps will be taken to help facilitate prospective tenants in their efforts to set up shop, this move is encouraging as the community looks for leadership, vision and creativity among its key stakeholders to improve conditions for retail commerce throughout the city for the long haul.

|

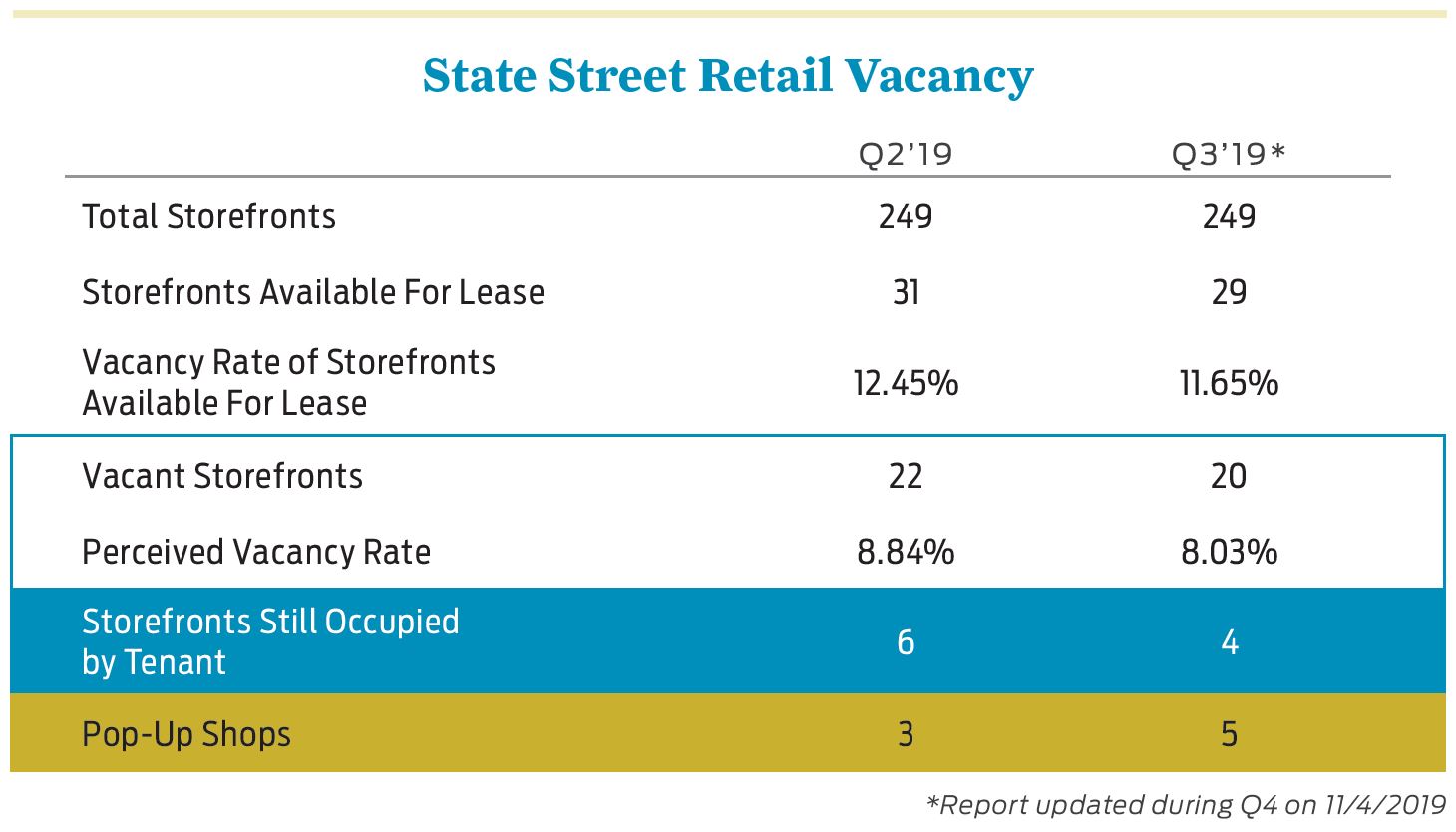

State Street Quarterly Retail Vacancy Update

Radius conducts a monthly visual inspection and research of the downtown State Street corridor (400–1300 blocks). Vacancy rates are calculated based on State Street-facing storefronts only, excluding first floor office spaces fronting State Street. Some spaces may be leased and we are not aware. Pop-up shops are included in the vacancy rate given their short term status.

Summary

-

-

- State-us quo continues. There has been very little overall change since the start of Q3 with 29 available storefronts for lease and 20 of those being vacant (just two fewer than the second quarter) which equates to a 8.03% perceived vacancy rate.

- New leases. There were 5 new retail leases totaling 9,726 SF signed from the start of the third quarter to date:

509 State St. — 2,824 SF (Pascucci / Leased in Q4)

907 State St. — 2,250 SF (Retail & Wholesale Inc.)

714 State St. — 1,917 SF (Luca B Styles)

430 State St. — 1,450 SF (Insomnia Cookies)

802 State St. — 1,285 SF (Thuy Dang) - New vacancies. Four storefronts totaling 9,478 SF became vacant during the third quarter:

509 State St. — 3,300 SF (Alito’s / Leased to Pascucci in Q4)

833 State St. — 2,500 SF (Wendy Foster / Moved to 1220 State St.)

801 State St. — 1,860 SF (Brauthaus)

931 State St. — 1,818 SF (LF Brand)

-

|

Q3 Multifamily Investments Summary: South Santa Barbara County

The South Coast multifamily market continues to see unprecedented demand. With very little inventory, the market is extremely competitive and quality properties have garnered multiple offers with prices sometimes over asking and with very aggressive terms. With increased vacancy risk in other commercial property types, the buyer pool for multifamily buildings in our area has widened. Several trophy assets such as 1501 Santa Barbara St. have been purchased by 1031 exchange investors seeking stability, and with an already substantial amount of local and institutional investors desiring assets here, average cap rates are at record lows. Interest rates have also dropped to levels not seen since 2016, making more deals pencil out than in the last few years.

Although the market continues to chug along with sellers having no problem getting top dollar for their assets, the elephant in the room is AB 1482. While the impacts of this state bill have not yet been fully solidified, changes have already begun to occur. Owners who have recently purchased buildings are in some cases realizing that any rent increases they have made will have to be rolled back to March 2019 levels, negating the appeal of some purchases made on a pro-forma basis. Banks are already updating their underwriting standards due to the bill, and are underwriting assets at their rent effective March 31st, not current levels.

But despite the new rent control bill looming, Santa Barbara owners are not necessarily lining up to sell, and when they do, they are having no problem getting top dollar for their assets. The fact remains that the South Coast will continue to be an extremely desirable place to live and work, and with barriers to entry remaining in place for additional housing, rents will continue to increase and vacancy will remain low.

The tightest of all Central Coast markets this year has been Isla Vista. A longtime favorite for local and institutional investors, this market has seen no inventory with only one sale at 6679 Abrego Rd. which was purchased by a local investor for $4,100,000. With the new rent bill in place, student housing could potentially provide a shelter against rent caps, since it is more common for students to relocate each year, leaving landlords open to increased rents. This could potentially make Isla Vista an even more attractive option for investors, increasing competition and prices for these assets.

The West Beach neighborhood also continues to shine with prices and yields generally well above the average for Santa Barbara. The proximity to the ocean, Funk Zone and Santa Barbara City College continues to drive demand for rentals, and many investors are focused on finding assets in that part of the city. The most recent sale was an 11 unit property which sold off market for $4,795,000 at a high 3% cap rate. Another property in a similar location was Montecito Gardens, which has commanded a great deal of attention from investors. With rents below market, it will be interesting to see how the investment pans out with AB 1482 now in place.

Recent News

Santa Barbara News-Press: American Riviera Bank buys Ventura property for its first full-service branch in Ventura County

American Riviera Bank established its first full-service branch in Ventura County. The bank purchased 1220 S. Victoria Ave., continuing its expansion along …

Noozhawk: Santa Barbara Community Weighs in on Proposed State Street Plan

When it comes to State Street, largely considered the heart of downtown Santa Barbara, everyone has an opinion. With the Santa Barbara City …

edhat: Santa Barbara South Coast Commercial Real Estate Sets Record at $361 Million

This marks the strongest performance recorded in the first quarter. Despite the record number, the largest came from two deals: first, the …